As a medical skilled, you’ve got doubtless shouldered a mountain of pupil debt to earn your white coat. For years, IDR and PSLF offered aid. However with the One Large Stunning Invoice Act (OBBBA), signed July 4, 2025, the panorama has modified. New federal borrowing caps, fewer reimbursement choices, and the gradual erosion of some forgiveness perks have extra debtors contemplating privately refinancing their pupil loans. Particularly now, because the SAVE curiosity freeze ended on August 1 and rates of interest are trending downward.

When you’re a physician, dentist, or excessive earner with mortgage-sized pupil loans who’s questioning about refinancing, this information breaks all of it down.

Privately Refinancing Eliminates Federal Protections

If you have already got a non-public mortgage and also you’re seeking to refinance it once more, it is sensible to take action anytime you’ll be able to decrease the rate of interest. Nonetheless, should you’re changing federal loans to non-public loans, it’s important to contemplate the federal protections that can go away. As soon as a federal mortgage is refinanced into a non-public mortgage, you’ll be able to by no means convert it again to federal. Listed here are the important thing federal protections.

- Deferment or forbearance: Federal loans provide deferment and forbearance choices, though curiosity typically accrues and OBBBA lower discretionary forbearance from three years to 9 months. Personal lenders not often present the identical flexibility.

- Revenue-driven reimbursement plans and normal reimbursement program: Federal loans provide IDR plans, which may preserve funds inexpensive throughout coaching. In contrast, non-public refinancing locks debtors into fastened reimbursement phrases that could be far costlier as soon as coaching ends.

- Loss of life and incapacity discharge: Federal loans are discharged if the borrower dies or turns into completely disabled—protections that many non-public lenders don’t match. Learn the advantageous print earlier than refinancing, or else your loved ones may very well be on the hook on your loans.

- Public Service Mortgage Forgiveness and IDR forgiveness: Federal forgiveness applications like PSLF can save physicians a whole bunch of hundreds of {dollars}, however when you refinance, these choices are gone. Make sure you are making the appropriate selection earlier than refinancing.

Extra data right here:

Past PSLF: The Prime Pupil Mortgage Compensation Options for Docs

Nervous In regards to the Authorities Taking Away PSLF? Begin a PSLF Aspect Fund

Who Ought to Refinance Pupil Loans Now?

There are a few frequent eventualities I see for many who ought to contemplate refinancing their pupil loans now.

Personal Follow Physicians

When you’re in a non-public observe or non-public group, you often don’t have any shot at PSLF. When you work in pharma or for an insurance coverage firm, these are additionally privately held organizations, and you will not qualify there both. There are two exceptions to the rule. First is an MD/DO/DPM working in California and Texas. There was a rule change a number of years in the past that granted PSLF eligibility for docs contracted to work at nonprofits (i.e., Kaiser, Sutter, even locums).

The opposite section that might delay refinancing is these contemplating the dreaded IDR forgiveness. IDR forgiveness may enchantment to those that

- Work part-time (or much less) or

- Work at a corporation that does not qualify for PSLF.

In addition they have to have pupil loans which are 2x, 3x, or 4x their revenue. I do not like this program in any respect since it’s a minimum of a 20-year dedication, the forgiven steadiness is taxable, and it is topic to alter. I’ve chatted with fairly a number of docs who had been pursuing an IDR plan known as PAYE that reached forgiveness in 20 years after which discovered they’d be compelled into IBR with the next month-to-month fee and 5 further years of funds. Yikes. Evidently, there are only a few white coat buyers who ought to look into IDR forgiveness.

Most working in non-public observe/teams will get monetary savings by refinancing their loans from the federal authorities to non-public.

Physicians with Smaller Balances

Those that owe lower than $100,000 can often pay it off rapidly, and so they will not profit a lot from forgiveness applications. There are a number of exceptions, corresponding to those that practice for eight-plus years (cardiology, CT surgical procedure, or peds surgical procedure) or who’ve an revenue lower than $200,000. In any other case, with a mortgage steadiness that low, you may be higher off refinancing and paying it off in lower than 5 years. Most will pay it off in a yr or two and never essentially need to reside like a resident.

Physicians with Aggressive Compensation Targets

Some docs I work with simply need the debt gone as rapidly as attainable. I encounter eventualities the place the physician would save some huge cash by doing a forgiveness program, however they resolve in opposition to it. Normally, it has to do with them not trusting the federal government or feeling responsible for pursuing a forgiveness program. Reasonably than paying your loans at 7%-9%, refinancing to a decrease fee could prevent hundreds in curiosity.

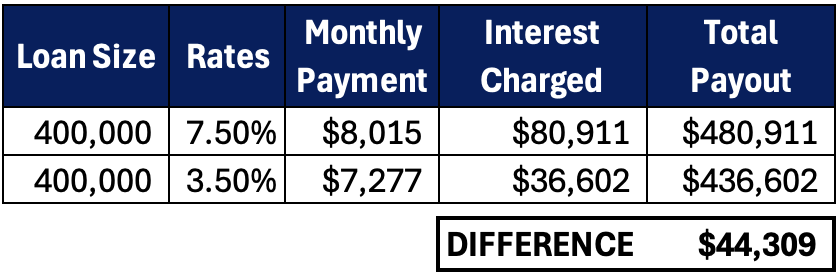

Here is an instance of a physician who refinances $400,000 at a 7.5% federal fee to a 3.5% non-public fee over a five-year time period.

This doc would save $44,309 in curiosity over 5 years in comparison with staying federal.

Who Ought to Assume Twice Earlier than Refinancing Pupil Loans?

Suspending refinancing shouldn’t be a foul thought for these two teams.

Physicians in Coaching

Whereas in coaching, it’s nearly at all times higher to maintain your loans federal. Funds could be inexpensive—$200-$400 per 30 days in an IDR plan. Plus, chances are you’ll be unsure concerning the job you may be taking after you graduate from coaching. When you’d favor to pay greater than the required IDR fee, you are able to do so to assist curb the curiosity. Those that have already signed a suggestion with a non-public observe or have a partner or associate who might help help them with the funds can contemplate refinancing whereas in coaching. Simply be completely sure you will not remorse passing up PSLF.

Physicians Unsure in Profession Paths

When you’ve got any uncertainty about whether or not you may keep at your non-public group or non-public observe, you possibly can maintain off on refinancing your pupil loans. Holding PSLF eligibility may change into a precious choice. In accordance with a 2023 survey from MGMA and Jackson Search Group, physicians who accomplished residency or fellowship within the six years prior had been spending lower than two years on common of their first job earlier than leaving. Furthermore, I’ve met with a number of docs who thought they had been dyed-in-the-wool non-public observe docs and ended up going again to hospital employment after a yr. The underside line is to maintain your loans federal and forgiveness as an choice till you are sure you may be out of public service for good.

Extra data right here:

The Case for Ending PSLF — And What You Ought to Do

Compensation Help Plan (RAP) Helps Early-Profession Physicians

The OBBBA shook up reimbursement plans for federal pupil loans. The Compensation Help Plan (RAP) was created as the most recent iteration of IDR plans. RAP opens on July 1, 2026, and it is an choice for any federal borrower. It is the one IDR plan for many who borrow or consolidate a federal mortgage on July 1, 2026, or later.

The RAP plan has an curiosity subsidy part that mirrors IDR predecessors corresponding to SAVE and REPAYE. Funds in RAP begin at a minimal of $10 per 30 days for an Adjusted Gross Revenue (AGI) below $10,000, and it scales upward in 1% increments per $10,000 bracket (e.g., 1% of AGI for $10,000-$19,999, rising to 10% for $100,000 or extra). An curiosity subsidy is utilized in case your month-to-month fee in RAP shouldn’t be sufficient to cowl the month-to-month curiosity. And it pays $50 towards the principal steadiness of the mortgage. Here is an instance of a resident doctor.

Dr. Patel owes $343,000 at a 7% rate of interest. Her curiosity is $2,000 per 30 days, and her fee in RAP is $400 per 30 days. Every month, she makes her required $400 fee, and $1,600 in unpaid curiosity is waived. With the curiosity profit, it retains her mortgage steadiness from rising, and $50 is utilized to the principal every month. Her equal rate of interest after the curiosity subsidy is utilized is 1.40% ($400 * 12 / $343,000). Meaning her fee whereas in RAP throughout that yr in coaching is 1.40%. It is unlikely she may refinance her mortgage to a decrease rate of interest than that.

Low sponsored charges would happen throughout coaching and even into the primary yr or two of observe as a result of delay with IDR recertification. Nonetheless, when you certify revenue with a full yr’s attending wage and even the half trainee/half attending yr, it is best to look into refinancing your pupil loans to a decrease fee because the subsidy is probably going phased out. You solely transfer ahead with the refinance should you’ve dominated out any probability at pursuing PSLF.

Rates of interest have been trending downward currently (and the Fed lower charges by 25 foundation factors earlier this month), and so they could proceed in that path subsequent yr after present Federal Reserve Chair Jerome Powell’s time period expires in Could 2026. With the SAVE curiosity freeze over, now is a superb time to contemplate refinancing your pupil loans to a decrease rate of interest. Earlier than you refinance, run the numbers and be sure PSLF isn’t a greater match. If you’d like assist evaluating, schedule a session with StudentLoanAdvice.com. When you’re able to refinance now, get a quote immediately with considered one of WCI’s vetted assets.

Pupil mortgage rates of interest are falling, and refinancing may very well be the appropriate transfer for you. When you undergo our affiliate hyperlinks within the chart under, you’re going to get the bottom charges accessible whereas additionally getting a whole bunch of {dollars} in money again.

† Bonus contains money rebates and worth of free course. Debtors who refinance greater than $60,000 in pupil loans utilizing the WCI hyperlinks will likely be enrolled in The White Coat Investor’s flagship course, Hearth Your Monetary Advisor: ATTENDING free of charge ($799 worth). Debtors will nonetheless obtain the wonderful money rebates that WCI has negotiated with every lender. Supply legitimate for mortgage functions submitted from Could 1, 2021 via April 30, 2026. Free course should be claimed inside 90 days of mortgage disbursement. To say free course enrollment, go to https://www.whitecoatinvestor.com/RefiBonus.

What do you suppose? Have you ever refinanced your loans currently? Are you contemplating refinancing your loans now? Why or why not?

– Funding Moats")

Makes NYSE High Gainer Record on Second Quarter Outcomes")

{kind=link}