Entire life insurance coverage is usually marketed as extra than simply life insurance coverage; it’s pitched by commission-seeking brokers as a wealth-building software with assured advantages, tax benefits, and money worth progress. On the floor, it could sound like an awesome monetary technique.

Supporters of complete life insurance coverage typically spotlight its ensures:

- Assured premiums,

- Assured demise profit, and

- Assured money worth accumulation.

For some individuals, particularly those that are risk-averse or dislike the volatility of the inventory market, this will really feel like a protected place to park cash. The issue is that security comes at a value: unfavorable preliminary and modest long-term returns. Modest returns on a big portion of the portfolio MUST be paired with a large financial savings charge with a view to attain your targets. The identical ensures that present security come at a price—particularly, a misplaced alternative. {Dollars} allotted towards a everlasting life insurance coverage coverage may have been invested elsewhere—reminiscent of within the inventory market, the place the potential for long-term progress is usually a lot larger.

Skeptics, and there are a lot of, appear to hate this monetary product greater than some other, nevertheless it has its legit makes use of. Let’s take a better take a look at complete life insurance coverage—together with the professionals, cons, and monetary realities—so you may resolve if and the way you would possibly use it.

TL; DR Model

The quick model of this submit is that you’ll in all probability neither want nor even need an entire life insurance coverage coverage when you perceive the way it works. Largely, these insurance policies are designed to be bought (for enormous commissions), not purchased. Most white coat traders have a a lot better use for his or her cash, whether or not that is paying down debt, maxing out retirement accounts, or investing aggressively. There are a number of fully cheap area of interest makes use of for complete life insurance coverage, even when simply being a physician will not be one in all them. Nonetheless, for the reason that buy of an entire life insurance coverage coverage is, like marriage, a lifelong monetary dedication, it needs to be approached with the same quantity of due diligence.

Notice that the choice to cancel an entire life insurance coverage coverage that maybe it’s best to by no means have purchased will not be the identical as the choice to keep away from the acquisition within the first place. The low returns on a coverage are closely front-loaded, so typically it is smart to carry on to a coverage you by no means ought to have purchased. Be sure to have any wanted time period life insurance coverage in place previous to cancelling an entire life coverage.

What Is Entire Life Insurance coverage?

Entire life insurance coverage is a everlasting life insurance coverage coverage that gives a assured demise profit for all times and builds money worth. In contrast to time period life insurance coverage, which lasts for a set variety of years (sometimes 5-30 years), complete life insurance coverage by no means expires. The primary purpose it prices a lot greater than time period life insurance coverage is as a result of it’s going to finally pay out for everybody who buys and maintains a coverage. Most time period insurance coverage insurance policies by no means should pay something to a beneficiary, as a result of they expire earlier than the insured dies.

How Entire Life Insurance coverage Began

Entire life insurance coverage received its begin within the Nineteenth century, when life insurance coverage developed as a approach to offer monetary safety to households after the demise of a breadwinner.

By the mid-Nineteenth century, insurance coverage firms, significantly mutual life insurers, started providing complete life insurance coverage as a approach to mix life insurance coverage safety with a financial savings mechanism. The thought was that policyholders may pay fastened premiums, accumulate money buildup, and obtain assured lifetime insurance coverage protection—a construction that appealed to these in search of each monetary safety and long-term wealth accumulation. The alternate options for funding for a lot of a long time afterward have been a lot much less engaging than what is obtainable as we speak.

Earlier than the Eighties, complete life insurance coverage made somewhat extra sense. It was an easier time: excessive commissions; no index funds; no Roth IRAs; no 401(okay)s; and restricted entry to low-cost, diversified investments. Most individuals didn’t have the instruments or information to successfully make investments available in the market. Entire life supplied a approach to construct financial savings in a tax-deferred, assured car with some pressured self-discipline. It wasn’t an awesome funding, however for a lot of, it was one of many higher ones accessible.

Issues are completely different now. At the moment, we now have entry to a plethora of economic instruments and funding autos that make it simpler than ever to develop wealth extra rapidly and at the least as tax-efficiently.

Entire Life Insurance coverage from Mutual vs. Inventory Firms

This evolution additionally led to 2 varieties of insurance coverage suppliers: mutual and inventory firms—every with distinct approaches to coverage possession, dividends, and money worth progress.

- Mutual firms (e.g., MassMutual, Guardian, New York Life): Owned by policyholders, these firms sometimes provide taking part complete life insurance policies that pay dividends, which may improve money worth or scale back premiums.

- Inventory firms (e.g., MetLife, Prudential): Owned by shareholders, complete life insurance policies from these firms are sometimes non-participating, that means they develop based mostly on assured curiosity and don’t pay dividends. Nonetheless, some inventory firms do provide taking part complete life insurance policies—typically via legacy coverage blocks or specialised product strains, which may pay dividends that improve money worth progress. Due to this variability, it is vital to rigorously assessment every coverage’s dividend standing and construction.

At first look, it’d seem that one ought to all the time buy insurance coverage from a mutual firm, however that’s not all the time the case. There may be way more nuance to this subject than could first seem. The specifics of the coverage matter as a lot, if no more, than the construction of the corporate standing behind it.

How Entire Life Insurance coverage Works

Entire life insurance coverage has some distinguishing options.

Mounted Premiums

The funds will keep the identical for all times, however they’re much larger than time period life insurance coverage.

Assured Demise Profit

The demise profit will likely be paid irrespective of while you go away, so long as premiums are paid.

Money Worth Development

A part of the premium builds tax-deferred financial savings, which will be borrowed towards or withdrawn. Notice that this money worth will not be separate from the demise profit. Accessing it through coverage loans or partial surrenders reduces the demise profit accordingly.

Dividends

Some insurance policies from mutual insurance coverage firms pay non-guaranteed dividends, which can be utilized to develop the coverage’s money worth and demise profit or may even be taken and spent as a non-taxable, “return of premium” money cost. A dividend rate of interest (DIR) is the speed mutual life insurance coverage firms use to calculate dividends paid to eligible complete life policyholders. These dividends aren’t assured, however when declared, they mirror the corporate’s total monetary efficiency—together with funding returns, mortality expertise, and working bills. Policyholders can use dividends in a number of methods:

- Scale back premiums

- Take as money funds

- Buy extra paid-up insurance coverage

- Depart them on deposit to earn curiosity

Notice that illustrations proven by a promoting agent usually assume these dividends are reinvested into the coverage by buying extra paid-up insurance coverage. Whereas the DIR provides a basic concept of how a coverage could carry out, the precise dividend quantity depends upon the specifics of every coverage. Notice that the DIR will not be the identical because the return in your “funding” of coverage premiums paid. It typically takes 5-15 years or extra to “break even” on an entire life “funding” regardless of being paid dividends annually.

Not All Everlasting Insurance coverage Insurance policies Are Entire Life Insurance coverage

There are different varieties of everlasting (lifelong) insurance coverage insurance policies, together with variable life insurance coverage and numerous varieties of common life insurance coverage. These insurance policies work otherwise from complete life insurance coverage. They might provide extra flexibility, however they often provide considerably fewer ensures. Additional dialogue of their nuances is past the scope of this submit, however the identical basic stage of warning needs to be utilized to their buy as with complete life insurance coverage.

Benefits of Entire Life Insurance coverage

Entire life does have some benefits over a time period life coverage.

Lifetime Protection

Time period life expires after a set interval, and in the event you attempt to renew it, the premiums skyrocket, so most individuals let it lapse. Entire life, however, is considerably costlier upfront, however the premium stays stage and the protection lasts your total life so long as you retain paying.

Money Worth Accumulation

Money worth builds over time, and it grows in a tax-protected method. It may be borrowed towards or withdrawn. Development is assured at a minimal charge.

Tax-Advantaged Partial Surrenders

You may partially give up a coverage, permitting you to entry money worth in a tax-advantaged approach. Notice {that a} partial give up means your demise profit (and in addition premiums due sooner or later) are lowered. When partially surrendering a coverage, the money is accessed utilizing the “First-In, First-Out” (FIFO) technique moderately than the “First-In, Final-Out” (FILO) technique utilized by annuities. Which means withdrawals are taken from the idea or principal (the entire of premiums paid) first (tax-free) earlier than accessing any positive factors (totally taxable at your extraordinary earnings tax charges). This tax benefit is exclusive to everlasting life insurance coverage.

Loans

One other technique of accessing the money worth is to borrow towards the worth of the coverage at pre-determined phrases. Whereas this will present entry to funds, it is vital to know that curiosity on the mortgage is usually paid to the insurance coverage firm, not again into your coverage. Though you are borrowing towards your individual money worth, the insurance coverage firm treats it as a mortgage utilizing your coverage as collateral. Some insurance policies provide a characteristic often known as “non-direct recognition” of coverage loans, and in the event you plan to entry your money worth through loans, that is typically a vital characteristic in your coverage. With non-direct recognition, your coverage, in essence, continues to pay dividends as if you had not borrowed towards it.

Assured Development

Development within the coverage money worth is assured at a really low charge. Whereas insurance policies often outperform the assured charge, calculating the “return on funding” of your premiums paid generally is a sobering expertise, even when the coverage is held for a lot of a long time. Two % per yr wouldn’t be uncommon.

Mounted Premiums

Like with a stage premium time period coverage, complete life premiums stay stage all through the coverage.

Potential Dividends

Some insurance policies pay dividends that can be utilized to scale back premiums, improve money worth, or be taken as money. Dividends should not assured and are depending on firm efficiency, however they’re often non-taxable, as they characterize a return of premiums paid.

Asset Safety

In some states, complete life insurance coverage money worth is protected against collectors in a chapter scenario.

Disadvantages of Entire Life Insurance coverage

As you have got in all probability guessed, there are an entire lot of drawbacks to complete life insurance coverage as nicely.

Excessive Premiums

Entire life insurance coverage prices considerably greater than time period life for a similar demise profit within the quick time period. For instance, a $1 million 20-year time period coverage for a 35-year-old may cost $700 yearly, whereas a $1 million complete life coverage may price as a lot as $15,000 per yr, greater than 20 instances as a lot. In different phrases, you may both purchase a $100,000 complete life coverage or a $2.1 million time period life coverage for a similar value. A type of will present dramatically extra profit to your heirs within the occasion of your premature demise. Thus, we see suggestions for “purchase time period and make investments the remaining.” If you happen to really make investments the distinction in premiums in some form of cheap method, you’re extremely prone to come out forward.

Low Funding Returns

The “return on funding” (not counting the worth of the insurance coverage) of your complete life premiums, even when held for many years, is prone to be within the vary of two%-5%—a lot decrease than inventory market returns and, within the preliminary years, even decrease than typical bond returns. Relying on the coverage’s construction within the first 10-20 years, returns are sometimes unfavorable as a consequence of the price of insurance coverage and commissions. It is a horrible short-term funding and never that nice of a long-term funding UNLESS you extremely worth the everlasting demise profit or another characteristic.

Complexity and Restricted Flexibility

Many policyholders don’t totally perceive coverage mechanics. For instance, borrowing towards the money worth reduces the demise profit until the mortgage is repaid. There should not two swimming pools of cash; there’s just one. One other instance is that dividends are solely paid on the money worth, not your entire premium quantity paid.

Coverage Lapses, Give up Charges, and Satisfaction Surveys

Lapses and surrenders are excessive for a lot of insurance coverage merchandise. Many policyholders drop their insurance policies as a consequence of excessive prices.

Listed here are the lapse charges (in accordance with a 2005 research accomplished by LIMRA):

- Entire life: 25% lapse inside three years, 40% inside 10 years, and a majority (round 80%) earlier than any demise profit is ever paid.

- Common life: 88% of insurance policies don’t pay a declare as a consequence of lapse.

- Listed common life (IUL): Excessive lapse charges as a consequence of market volatility and rising prices.

- Time period life: Time period life additionally has excessive lapses, significantly on the finish of the time period. Ten % lapse yearly; end-of-term lapse happens on the finish of the extent premium interval, when time period charges skyrocket, with charges between 30%-50% and even larger relying on the size of the time period. In fact, a time period coverage lapsing when not wanted is much completely different from a everlasting coverage like complete life, which is designed to be held till demise, lapsing. Upon lapsing, any positive factors in an entire life insurance coverage coverage are taxable at extraordinary earnings tax charges, eliminating a lot of the good thing about the prior a long time of tax-protected progress.

Casual surveys of white coat traders have instructed that 75% of those that have bought an entire life coverage remorse the acquisition. Feedback left on this web site, in WCI boards, and in emails recommend a frustratingly excessive variety of medical doctors have bought/been bought complete life insurance coverage inappropriately.

Ought to Medical doctors Purchase Entire Life Insurance coverage?

There are conditions the place complete life could also be an appropriate choice. These are virtually all conditions the place a everlasting, lifelong demise profit is required or at the least desired. When evaluating options for the wants outlined beneath, it’s vital to contemplate all accessible choices, however do not anticipate to listen to in regards to the different choices from an insurance coverage agent.

Tax-Environment friendly, Liquid Property Planning Ensures

In case your property will likely be massive sufficient to generate both federal or state property taxes, it’s possible you’ll want to transfer belongings into an irrevocable belief so future appreciation is outdoors of the property. Life insurance coverage is usually used to fund these trusts, known as Irrevocable Life Insurance coverage Trusts (ILITs), for 3 causes. The primary is the assure. Investments take time to develop, even when they’ve a better anticipated return than life insurance coverage on the grantor’s (funder of the belief) life expectancy. If the grantor dies early, the life insurance coverage will nonetheless guarantee a big sum of money within the belief. The second purpose is simplicity and tax effectivity. Not solely is a life insurance coverage demise profit tax-free (and investments in an irrevocable belief don’t get a step up in foundation at demise), nevertheless it grows in a tax-protected approach till then. The third purpose is liquidity. Life insurance coverage demise advantages are paid out in money, which can be utilized to pay property taxes or different bills extra simply than illiquid belongings like actual property or non-public companies (which can even be a part of the property). This liquidity characteristic can also be typically used outdoors of an irrevocable belief for very illiquid estates, like a big household farm that may should be bought to offer inheritances for a number of heirs or to pay property taxes.

Alternate options to contemplate: Conventional investments, gifting methods, assured common life, credit score strains, trusts, staggered liquidation of belongings.

Enterprise Proprietor Purchase-Promote Agreements

Entire life insurance coverage ensures a payout for buy-sell agreements, ensuring that enterprise companions should purchase out a deceased proprietor’s share so they don’t have to be in enterprise with the heirs or, even worse, promote or shut the enterprise. Purchase-sell incapacity insurance coverage insurance policies may also be bought for comparable functions.

Alternate options to contemplate: Time period life insurance coverage, buyouts over time, assured common life.

Key Individual Insurance coverage

For companies reliant on a particular particular person, life insurance coverage can present funds to interchange them or to interchange misplaced worth for the heirs. Whereas time period life can be utilized throughout typical working years, complete life could also be a very good choice for older key staff, as time period life can grow to be prohibitively costly after age 60.

Alternate options to contemplate: Time period life insurance coverage, self-insuring (massive amount of money), assured common life.

Asset Safety

Whereas returns on an entire life coverage “funding” should not very excessive, some persons are keen to surrender returns to guard belongings in a chapter scenario. Folks shopping for complete life insurance coverage for that reason want to ensure 1) their state really protects complete life money worth in chapter and a pair of) they’ve already taken all different asset safety strikes acceptable for his or her scenario first, reminiscent of Roth conversions and asset safety trusts.

Alternate options to contemplate: Legal responsibility insurance coverage, homestead legal guidelines, retirement accounts, Roth conversions, household restricted partnerships, household LLCs, Deliberately Faulty Grantor Trusts (IDGT) reminiscent of Spousal Lifetime Entry Trusts (SLAT), home asset safety trusts, overseas asset safety trusts, annuities.

Bond Alternative

Even long-term complete life returns pale compared to these accessible from inventory index funds and well-managed actual property, however they don’t seem to be so completely different from bond returns, particularly for these in excessive tax brackets who should put money into these bonds in a taxable account. Whereas muni bonds pay federal (and typically state and native) tax-free curiosity, long-term returns in an entire life coverage could also be larger, particularly for many who do not anticipate spending the curiosity or principal from these bonds throughout their life.

Alternate options to contemplate: Bonds, asset location methods.

Offering for Dependents with Particular Wants

Life insurance coverage can assure a set quantity of funds for a particular wants little one or dependent, no matter when the insured passes away. Whereas a disabled inheritor can reside simply as nicely on the proceeds of a time period life coverage or your leftover nest egg, an entire life coverage is an affordable selection for this want, particularly for somebody who doesn’t grow to be financially impartial till late in life (or by no means) or has a small nest egg and is primarily residing on Social Safety or a pension in retirement. Whereas the nest egg can be accessible to the disabled inheritor, the Social Safety and pension wouldn’t.

Alternate options to contemplate: Time period life insurance coverage, conventional investments, ABLE accounts, particular wants trusts.

Juvenile Insurance policies in Households with Inherited Well being Points

If a baby has a household historical past of well being circumstances, an entire life coverage with a assured insurability rider may also help safe future protection, whereas time period life sometimes isn’t accessible for kids. Whereas it’s usually a mistake to purchase life insurance coverage on somebody if no one depends upon their earnings and whereas shopping for life insurance coverage on youngsters is usually an indication of economic illiteracy, there are a number of insurance policies on the market the place you’re primarily shopping for a considerable amount of assured insurability later moderately than a demise profit now. These are usually complete life insurance policies.

Alternate options to contemplate: Self-insure, search employment solely with employers providing life insurance coverage as a profit, convertible little one riders on parental time period insurance policies.

Pressured Financial savings with Ensures

Some people recognize stability, and complete life insurance coverage supplies a protected, predictable choice in comparison with market volatility. The tradeoff is doubtlessly lacking out on considerably larger returns that may very well be achieved by taking those self same {dollars} and investing in shares or actual property. Skeptics would argue that those that should be “pressured” to avoid wasting with required complete life premiums are additionally these almost certainly to let that coverage lapse anyway, resulting in dire penalties.

Alternate options to contemplate: Conventional investments, automated saving program, retirement accounts.

Charitable Gifting

Entire life insurance coverage can present a assured reward to a charity by naming it because the coverage beneficiary. The secret is that you need to worth the assure, as conventional investments are probably (however not assured) to depart extra to the charity. Life insurance coverage may even be utilized in Charitable The rest Trusts of conventional investments for comparable causes.

Alternate options to contemplate: Conventional investments, Donor Suggested Funds (DAF), charitable foundations, charitable trusts.

Financial institution on Your self/Infinite Banking

Some individuals use a specialised complete life coverage as an alternative of a financial institution. They use options like maximizing paid-up additions, non-direct recognition loans, and wash loans to attenuate commissions and the period of time required to interrupt even. Whereas there’s plenty of hype and salesmanship round these concepts, you’re mainly buying and selling poor short-term returns for larger long-term returns on money.

Alternate options to contemplate: Typical money investments reminiscent of high-yield financial savings accounts, cash market funds, and CDs.

When Entire Life Insurance coverage Might Not Be the Finest Alternative

Given the dimensions of the commissions supplied on these insurance policies (as a lot as 50%-110% of the primary yr’s premium), one shouldn’t be stunned to see brokers grow to be extremely motivated to promote them. It is essential to acknowledge if you’re one of many individuals who mustn’t purchase them. Let’s undergo these teams of individuals.

Nearly Everybody

Your default place when evaluating one in all these insurance policies needs to be that it’s NOT best for you as a result of it’s not proper for nearly everybody one and also you’re in all probability in that overwhelming majority. Simply being a physician or different high-income skilled or high-net-worth particular person will not be sufficient purpose to purchase an entire life coverage.

Physicians and Younger Professionals Needing Revenue Alternative

Entire life insurance coverage is usually bought inappropriately to early-career physicians with a number of higher makes use of for his or her cash. I take into account it monetary malpractice to promote a coverage to these with 5%-10% pupil loans. These docs typically do want strong life insurance coverage protection, however that ought to virtually all the time be supplied with time period insurance coverage. The entire following makes use of of cash are frequent for younger physicians and are usually higher makes use of of their cash than complete life insurance coverage:

- Create (or increase up) an emergency fund

- Repay bank cards

- Repay auto loans

- Exchange a beater automobile

- Repay pupil loans

- Max out Well being Financial savings Accounts (HSAs)

- Max out retirement accounts

- Do Roth conversions upon leaving coaching

- Save up a down cost for a mortgage

- Put money into inventory index funds in a taxable account

- Purchase funding actual property

- Put cash away for kids in 529s, UTMAs, or Trump Accounts

For these early of their careers, particularly physicians with excessive pupil mortgage debt, time period life insurance coverage is the extra reasonably priced selection. It supplies larger protection at a decrease price, permitting more cash to go towards mortgage reimbursement, investments, and retirement financial savings. Since most professionals solely want protection till they attain monetary independence (FI), time period life needs to be strongly thought of over complete life insurance coverage. If you happen to actually assume you may want an entire life coverage later, you may all the time add a conversion rider (it is typically free) to your time period life insurance coverage and later convert it to an entire life coverage with no medical examination in case your circumstances change and complete life turns into acceptable.

These In search of Increased Funding Returns

Entire life insurance policies construct money worth slowly, typically don’t break even for 10-15 years, and have modest returns even when held for years. If you happen to want your cash to do plenty of the heavy lifting to construct your retirement portfolio, it’s worthwhile to be investing in inventory index funds +/- actual property, not complete life insurance coverage. Conventional investments are prone to provide larger returns and extra flexibility.

Anybody Who Might Wrestle with Premiums

Entire life prices 10-20x greater than time period for a similar protection. If maintaining with premiums turns into troublesome, policyholders danger lapsing or surrendering the coverage, typically at a loss. If future affordability is a priority, time period life is the higher strategy. You don’t need a excessive premium-to-income or premium-to-savings ratio when shopping for these. If 1/4 or extra of your financial savings or greater than 5% of your gross earnings goes to complete life insurance coverage, you are in all probability shopping for approach too large of a coverage. Physicians who mistakenly decide to premiums of $30,000, $40,000, or extra per yr usually remorse the acquisition and find yourself surrendering the coverage at a loss inside a number of years.

Paying for School

Some brokers have even advocated buying complete life insurance coverage to pay for school (utilizing loans). The issue is that the period of time most dad and mom save for school is in regards to the period of time required for an entire life coverage to interrupt even. Most individuals simply want larger returns than that to fulfill their targets. Apart from, a 529 account presents much more tax benefits than an entire life coverage.

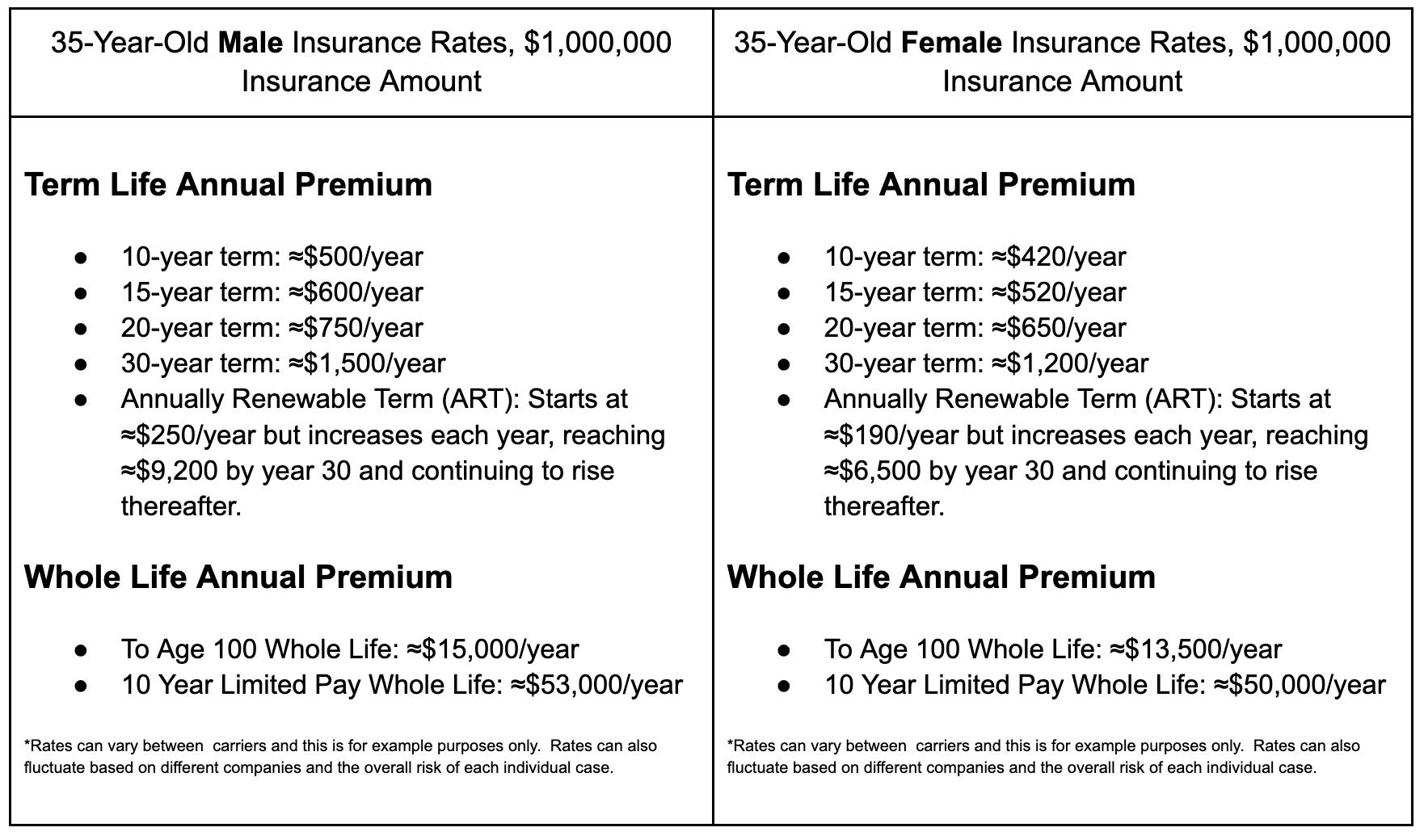

Evaluating the Annual Value of Entire Life vs. Time period Life Insurance coverage for a 35-Yr-Outdated (Most popular Danger Class)

The chart beneath exhibits the annual premium for a $1 million coverage on a 35-year-old “preferred-risk” (i.e., low danger) male or feminine. Females in the identical class pay barely decrease charges.

- Degree-term choices (10, 20, and 30 years), the place you lock in a set premium for your entire time period.

- Entire life choices provide completely different premium constructions. For this instance, a “to-age-100” plan, the place you pay annual premiums till age 100, and a “10-pay” plan, which carries considerably larger annual premiums however is totally paid up after 10 years.

Time period life is easy: decide your time period, and your premium stays stage all through the time period. With complete life, you select how lengthy you’d wish to pay, spreading prices over a lifetime or concentrating them right into a shorter interval—with the tradeoff that shorter pay-up intervals carry larger annual premiums. The next chart demonstrates how premiums change over time with the assorted varieties of time period and complete life insurance policies.

As you may see beneath, simply as incapacity insurance coverage is costlier for girls, life insurance coverage is cheaper. Ladies reside longer on common, even when they’re extra prone to grow to be disabled.

What Occurs When the Time period Life Insurance coverage Ends?

Time period insurance policies can sometimes be renewed as soon as the time period ends, however the premium will increase considerably:

- 10-year time period: In yr 11, the premium jumps to over ≈$5,000 and continues to rise yearly.

- 15-year time period: In yr 16, the premium will increase to over ≈$7,000 and rises annually thereafter.

- 20-year time period: In yr 21, the premium will increase to over ≈$10,000 and continues to rise yearly after.

- 30-year time period: In yr 31, the premium spikes to over ≈$36,500 and retains rising.

- Annual renewable time period: Continues to rise yearly.

Due to the sharp improve in price, most individuals select to not renew their time period coverage. The truth is, purchased appropriately (i.e., to cowl the interval till you hit monetary independence), it needs to be canceled earlier than the time period is up. Nonetheless, there are exceptions—particularly in instances of significant sickness or when new insurance coverage is not an choice and circumstances or poor planning meant there was nonetheless a necessity for a demise profit when the time period expired.

In distinction, the entire life premium will be stage for all times. For an aged particular person nonetheless paying premiums, complete life would possibly provide the bottom annual premium at a sure level.

A Actual-Life Instance

A person was identified with terminal colon most cancers simply earlier than his time period coverage was set to run out. He had been paying just some hundred {dollars} per yr for a $1 million coverage. When the time period ended, the premium jumped to almost $1,000 per thirty days. Though the price was steep, he and his spouse selected to proceed the protection. Given his analysis, he wouldn’t qualify for a brand new coverage, and his demise was imminent. In that scenario, paying the upper premium made sense, whether or not the insurance coverage was nonetheless wanted (on this case, it was).

Entire Life as a Retirement Technique

Entire life insurance coverage is usually pitched as a technique of saving for retirement, significantly to medical doctors who’ve already maxed out retirement accounts and do not realize that you could all the time make investments extra in a taxable account.

Notice that this use of complete life was not listed above as one of many “acceptable” makes use of for complete life insurance coverage. Any truthful comparability of complete life insurance coverage to saving for retirement utilizing retirement accounts and utilizing cheap assumptions exhibits such a dramatic benefit to the retirement account strategy that anybody selecting to skip a retirement account contribution to pay complete life premiums would appear like a idiot. Even outdoors retirement accounts, if you’re investing aggressively (largely shares and actual property) and tax-efficiently (index funds, low turnover, benefiting from depreciation to protect rental earnings, decrease long-term capital positive factors tax charges, decrease certified dividend tax charges, tax-loss harvesting, particular identification of excessive foundation shares when promoting to spend, utilizing low foundation shares for charitable donations, and so forth.), the benefit of conventional investments as a consequence of larger returns compounded over a few years can even be fairly evident.

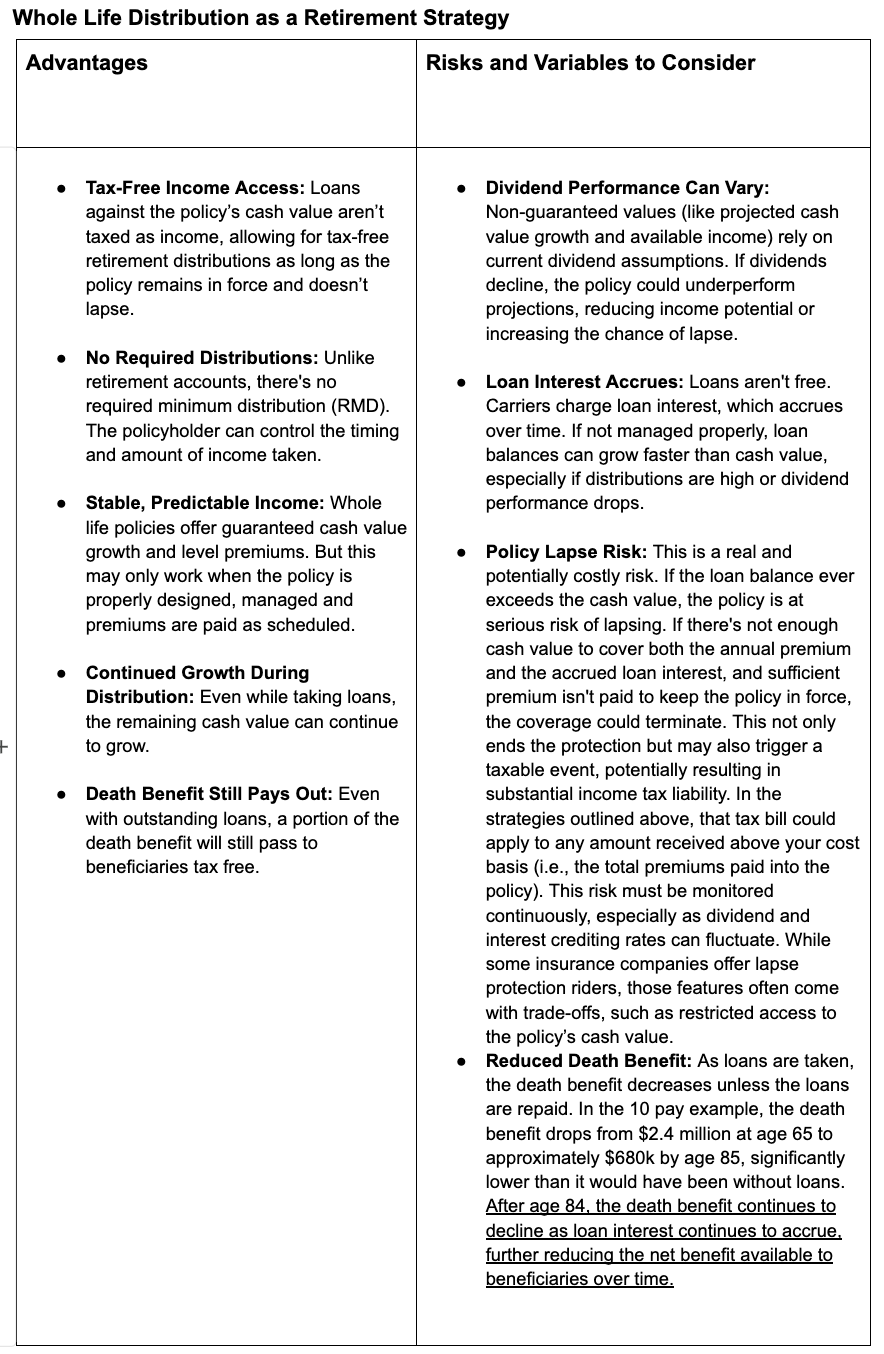

In fact, an entire life insurance coverage coverage works finest when designed for its anticipated use upfront. In case your purpose is to maximise your demise profit, design the coverage that approach from the start. If you happen to plan to borrow towards the money worth ceaselessly (together with to pay retirement bills), it needs to be designed to attenuate commissions, maximize money worth, and decrease the price of these loans utilizing options reminiscent of non-direct recognition of loans, paid-up additions, and wash loans. Whether or not you anticipate accessing the money utilizing partial surrenders (curiosity and tax-free however lowering the demise profit) or loans, the coverage needs to be designed to facilitate that technique. Sadly, too few purchasers of this difficult product ever hear about any of those options and the way they may influence coverage efficiency a long time from now. Frankly, too few sellers of this product perceive the influence of coverage design on future efficiency.

The first advantages of an entire life coverage come from its ensures. The extra you worth these ensures, the extra probably you’re to be proud of the coverage after buying it.

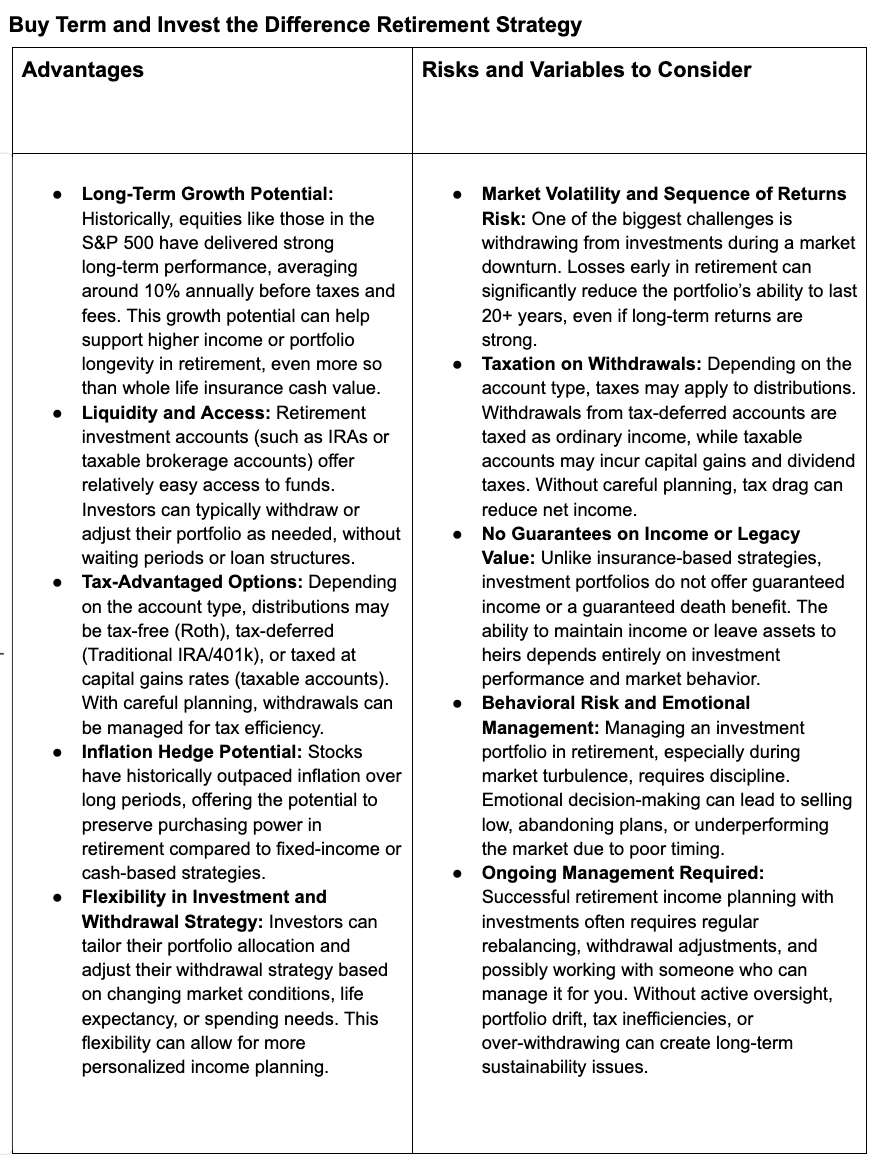

When evaluating complete life insurance coverage methods to a buy-term-and-invest-the-difference strategy, every presents distinct benefits relying on the person’s targets, danger tolerance, and monetary self-discipline. Entire life insurance coverage supplies everlasting demise profit safety, secure progress via assured values, and potential tax-advantaged entry to money worth, significantly later in life. Nonetheless, early money worth progress is usually sluggish, and long-term outcomes rely on non-guaranteed dividend efficiency. In distinction, the time period and funding technique can lead to considerably larger projected account values and larger flexibility, particularly when market returns align with historic averages. It additionally permits for the potential to generate substantial retirement earnings, although it lacks assured protection and carries extra publicity to market danger. In the end, these methods mirror completely different philosophies: one prioritizes ensures and lifelong insurance coverage protection, whereas the opposite is all about funding progress and management. There are tradeoffs on each side.

A easy comparability between an entire life coverage and a typical funding in a Roth account is well made. A “10-pay” complete life coverage with a $1 million demise profit could have an annual premium of $53,000 for 10 years. That $53,000 may be contributed to Roth accounts for 10 years through the Backdoor Roth IRA course of; the Mega Backdoor Roth IRA course of; Roth conversions; and Roth worker deferrals to 401(okay)s, 403(b)s, and 457(b)s. Whereas $53,000 may be greater than many individuals can get into Roth accounts in a given yr (with out conversions), Katie and I can presently contribute $185,000 to Roth accounts in a single yr. So, $53,000 is actually accessible to numerous individuals.

Over 30 years, that 10-pay coverage at present dividend scales would develop to $700,000 on the assured scale and $1.65 million on the projected scale. In the meantime, the Roth account rising at an annualized 8% return would develop to $3.58 million, over twice as a lot because the projected scale and 5 instances as a lot because the assured scale. The Roth cash will be accessed interest-free and tax-free in retirement. The entire life cash may solely be accessed through partial surrenders (which might decrease the demise profit) or through coverage loans (which cost curiosity), though each of these strategies would even be tax-free. As a retirement funding, the comparability is not even shut.

What the Roth account doesn’t present, in fact, is a demise profit. Nonetheless, so long as that demise profit will not be wanted after the preliminary 30 years, it’s simply bought utilizing an affordable time period coverage. Thus, it’s simple to see that if you’re not buying an entire life coverage since you place a excessive worth on the everlasting demise profit, you’re in all probability going to return out behind financially.

Benefits and Dangers of Entire Life Throughout Retirement Years

It’s not nearly what you accumulate by age 65—it’s about how successfully you may flip that worth into earnings you received’t outlive. This part takes a better take a look at how complete life insurance coverage and investment-based methods carry out when used as earnings sources in retirement, outlining the important thing benefits, potential dangers, and variables that may have an effect on long-term outcomes.

Annuities Are for Revenue

It is value noting right here that the insurance coverage product finest for offering assured earnings in retirement will not be complete life insurance coverage. It is really an annuity. Whereas complete life insurance coverage supplies money at demise, the basic earnings annuity insures towards you working out of money earlier than you die. Annuities will be bought with funds from any supply, together with a taxable account, a retirement account, or a 1035 alternate from the money worth of an entire life coverage.

The Backside Line

Far too many complete life insurance coverage insurance policies are bought with out correct schooling or understanding, and with commissions as excessive as they’re, brokers typically have a powerful incentive to make a sale. At The White Coat Investor, we consider in empowering you thru schooling. Entire life insurance coverage is a fancy product, combining ensures, charges, and long-term commitments. It hardly ever performs an vital position in sure monetary plans and solely while you totally perceive the way it works and the way it matches into your total technique.

For many physicians and high-income professionals, time period life insurance coverage mixed with disciplined investing can result in higher long-term progress. Entire life, however, will not be an funding, and it shouldn’t be handled like one.

That stated, in the event you totally perceive the construction, take consolation within the tradeoffs, and it aligns along with your long-term targets, purchase as a lot complete life insurance coverage as you need. The secret is knowledgeable decision-making, not one-size-fits-all concepts.

WCI-vetted insurance coverage brokers can reply your questions and provide help to make the suitable resolution if complete life is one thing you’re contemplating. They’ll inform you on the ins and outs of all life and incapacity insurance coverage choices. Before you purchase complete life, ask your self:

“Would I nonetheless need this coverage if I needed to hold it for a lot of a long time till demise?”

If the reply is not any, time period life might be the higher match.

Do you have got or have you ever had an entire life insurance coverage coverage? Has it labored out for you? What have been the advantages? What have been the downsides?

– Funding Moats")

Makes NYSE High Gainer Record on Second Quarter Outcomes")

")

{kind=link}