Lengthy-time readers know I’m an enormous fan of ready till 70 to take Social Safety. Clearly, there are exceptions to this common recommendation (i.e., typically it is smart for the decrease earner in a pair to take it earlier, these with decrease life expectancy ought to take it earlier, and so forth.)—it is all closely explored elsewhere on this weblog. Nonetheless, none of that’s truly the principle challenge of ready till 70 to take Social Safety.

The Drawback with Ready Till Age 70

The actual drawback is that too many individuals assume they should work longer or spend much less till they get to age 70. That’s NOT what I imply after I say delay Social Safety. The truth is, I believe it is truly a catastrophe if that occurs.

When individuals first retire, they enter what are referred to as the “go-go years” (adopted by the “slow-go years” and the “no-go years”). You truly wish to spend MORE cash, a minimum of in inflation-adjusted {dollars}, in these first few retired years than you do later. And in the event you retire earlier, that simply means you get extra of the go-go years. Feeling like you’ll be able to’t spend extra till you hit age 70 (the later go-go years and maybe into the slow-go years) is an actual drawback.

So, how will you wait till 70 for Social Safety however nonetheless spend extra within the years earlier than then? Properly, it’s a must to produce other cash. Forty p.c of retirees live on simply Social Safety. So that you can retire earlier than 70 and delay Social Safety till 70, it’s a must to have another supply of spending cash. Perhaps that is an inheritance or a working partner or one thing, however for many WCIers it’s (and needs to be) a nest egg. , that large pot of cash you spent your life buying. Constructing a nest egg that may assist you whenever you’re completed working is definitely the best monetary process of your life. These nest eggs are often seven figures, usually within the $2 million-$5 million vary and typically much more than $5 million. That is what you spend whereas ready to get your Social Safety test at age 70.

On this publish, we will speak about precisely how to try this.

Extra data right here:

8 Issues You Should Know About Social Safety

The Penalties of Ignoring Social Safety

What Will Social Safety Truly Pay?

Primarily, you are making an attempt to make use of some portion of your nest egg to switch Social Safety from the date of retirement till age 70, whenever you start taking Social Safety. An necessary variable in that calculation is the quantity Social Safety will truly pay you. You’d suppose this may be a straightforward quantity to search out since all of us get Social Safety statements yearly, proper? This is the chart from a current certainly one of mine.

This sort of does a superb job of demonstrating why it is good to attend till age 70 to begin Social Safety. That whole of $4,521 is far more cash than $2,423 (87% extra!), particularly contemplating that is doubtless the one assured supply of inflation-adjusted revenue obtainable to you. Nonetheless, it’s very deceptive. The chart in your assertion assumes you’ll work till the date your advantages start. The age 62 quantity assumes I will work till 62, and the age 70 quantity assumes I will work till 70, paying into the Social Safety system your entire time. When you retire at 60, your advantages most likely will not be that enormous.

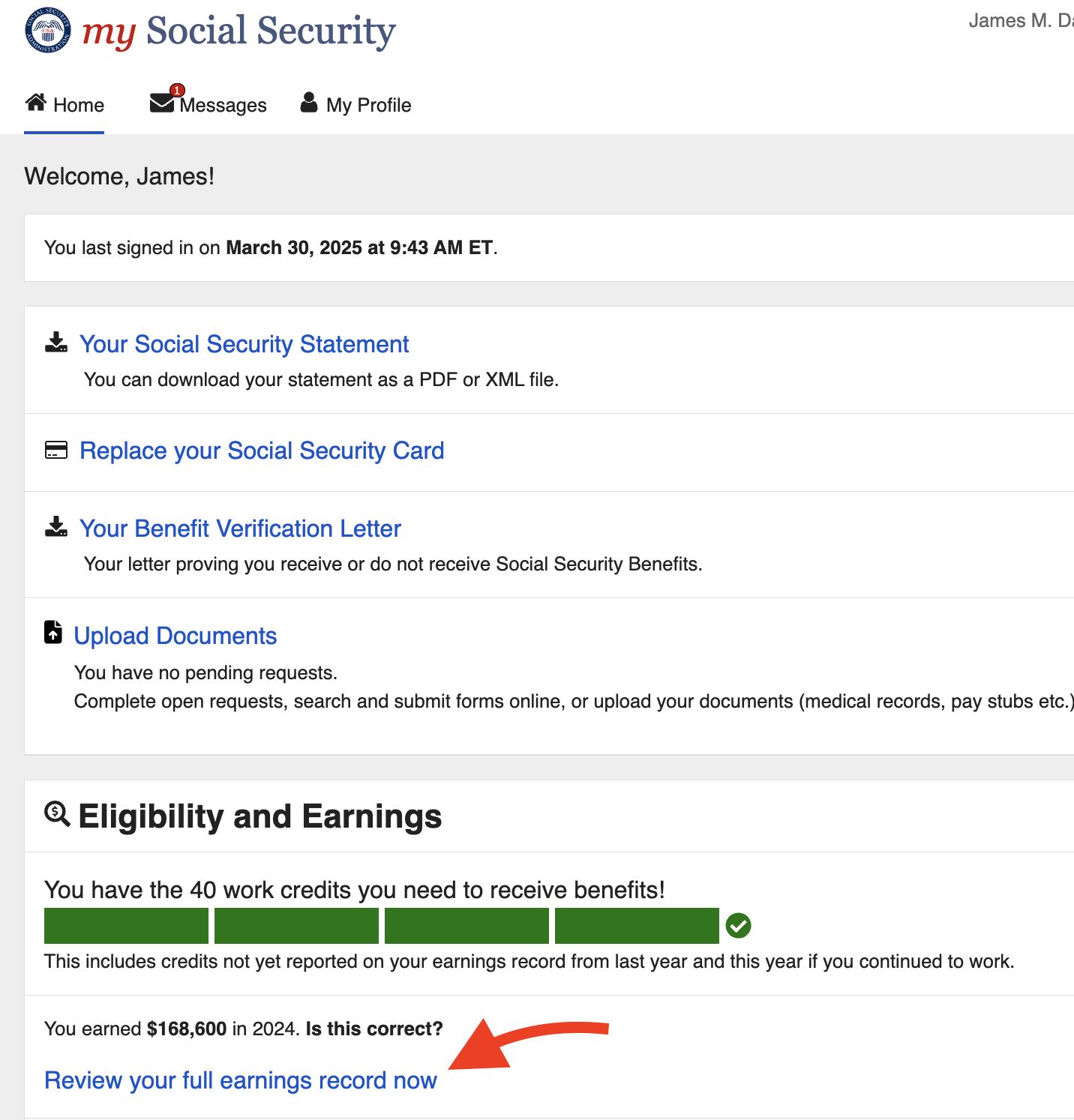

So, the primary process is determining what your Social Safety advantages will truly be. That requires a go to to 2 websites. The primary is the Social Safety web site. You log in utilizing a login.gov account, which you hopefully have already got. If not, go get one first. When you get there, you discover your earnings file by clicking on “Evaluate your full earnings file now.” (pink arrow)

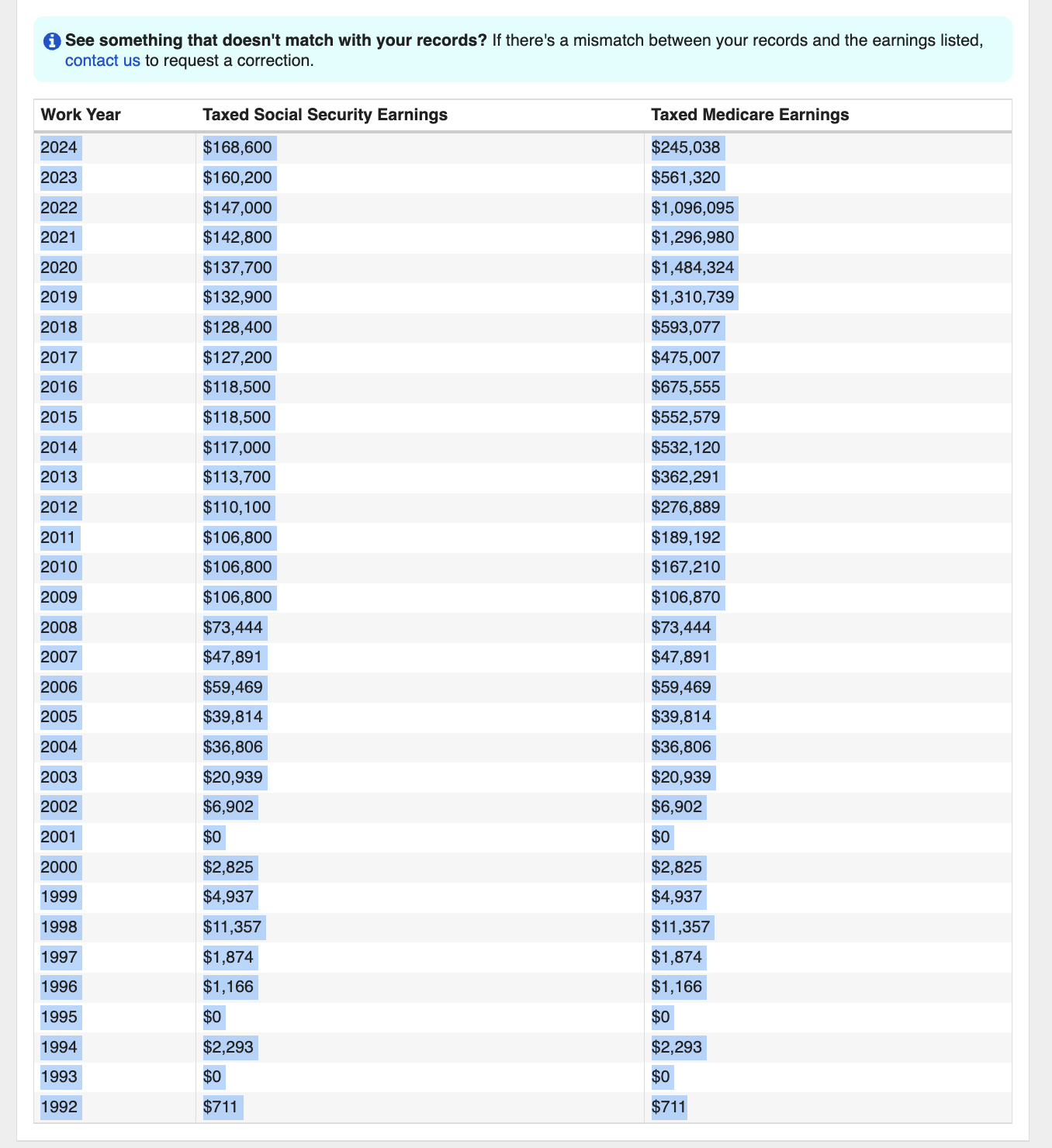

Your precise file will most likely look rather a lot like mine . . .

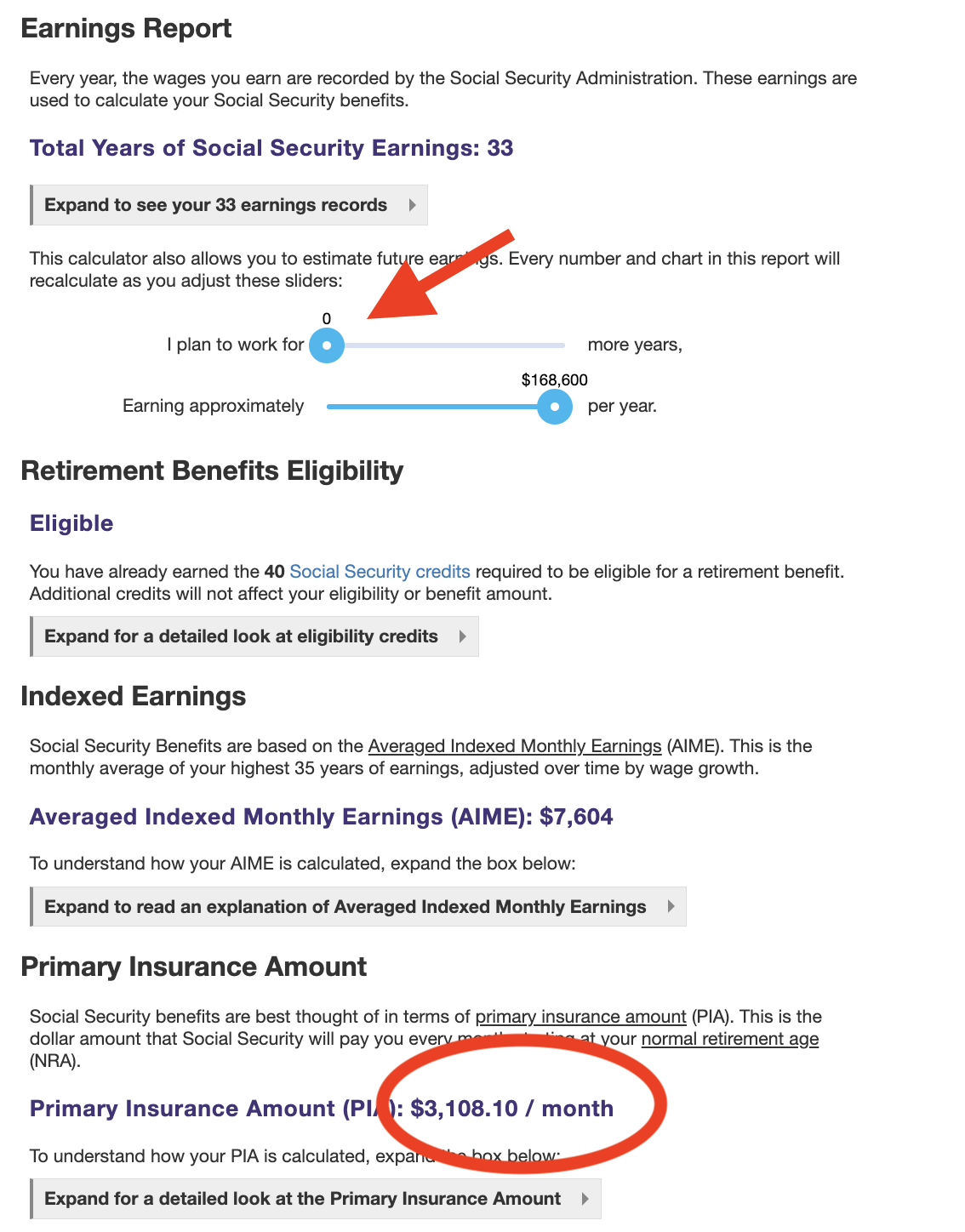

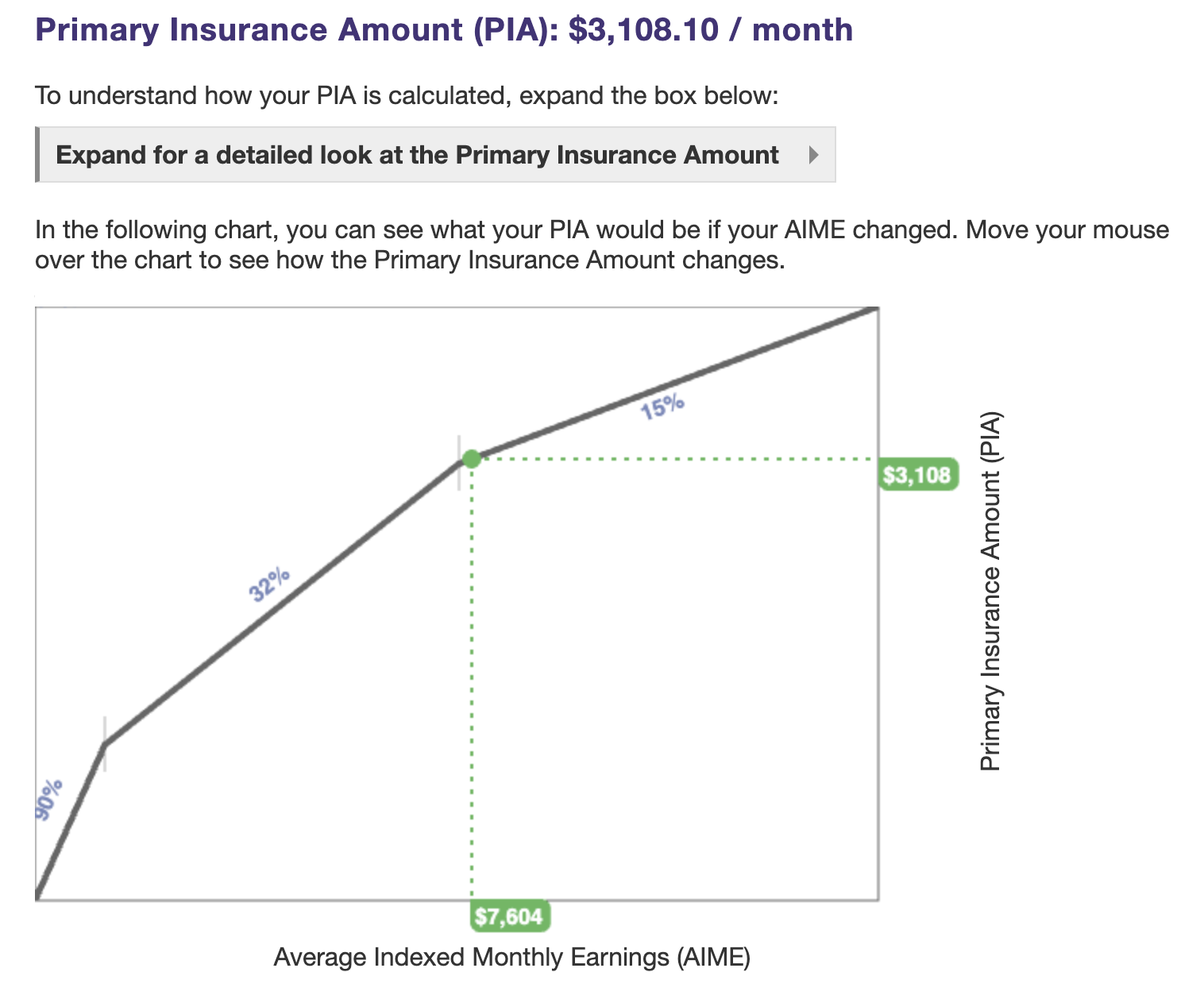

. . . which you then copy and paste right into a field at https://ssa.instruments/calculator. That may then spit out your Major Insurance coverage Quantity, or PIA (within the pink circle under).

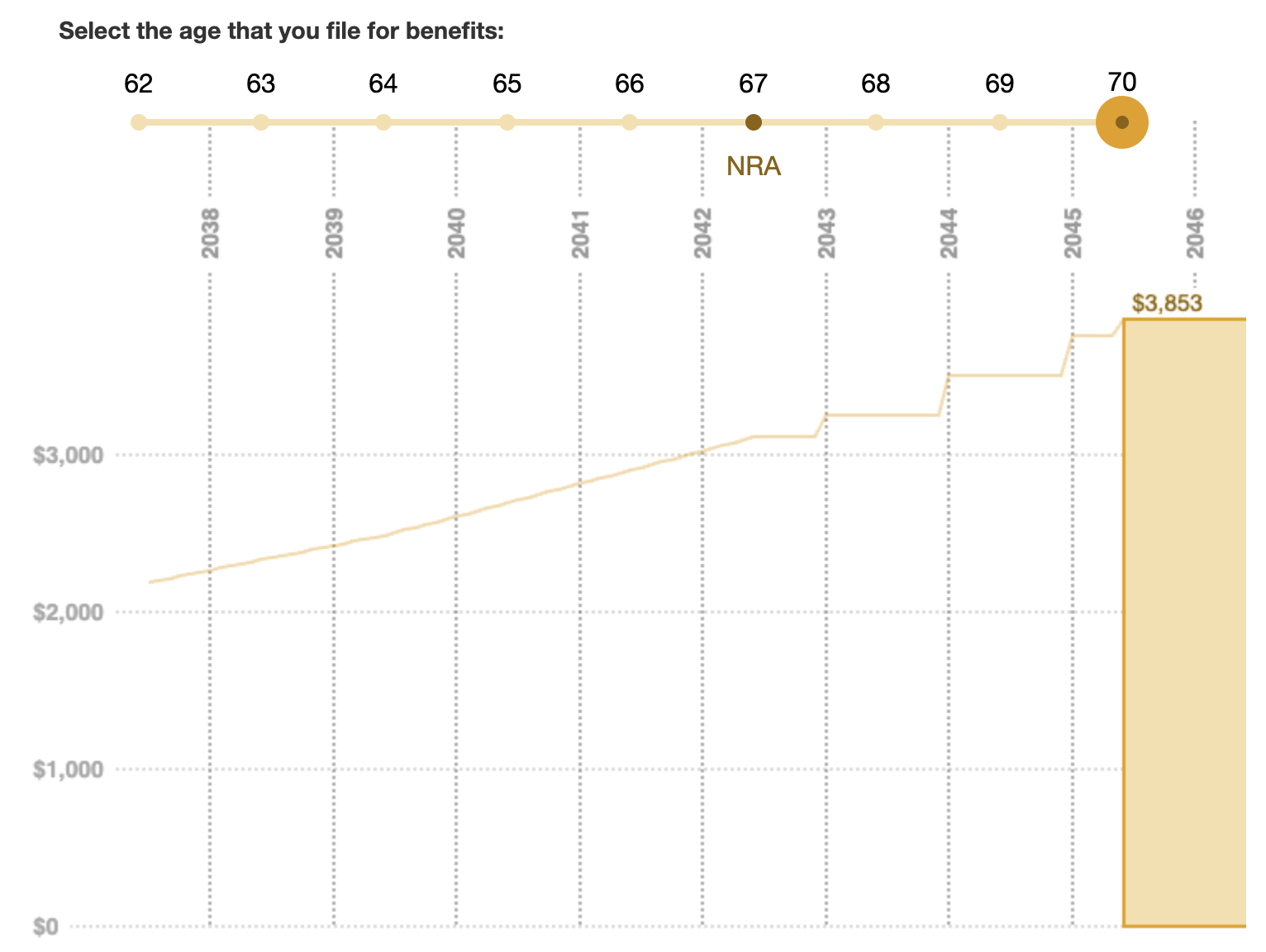

My PIA this 12 months is $3,108. After getting that, you modify the slider (pink arrow) on that very same calculator web page to working zero extra years, and it will then enable the choice to make use of a decrease slider on the web page to determine what your profit can be at age 62 and at age 70 in the event you by no means work (and pay Social Safety taxes) once more.

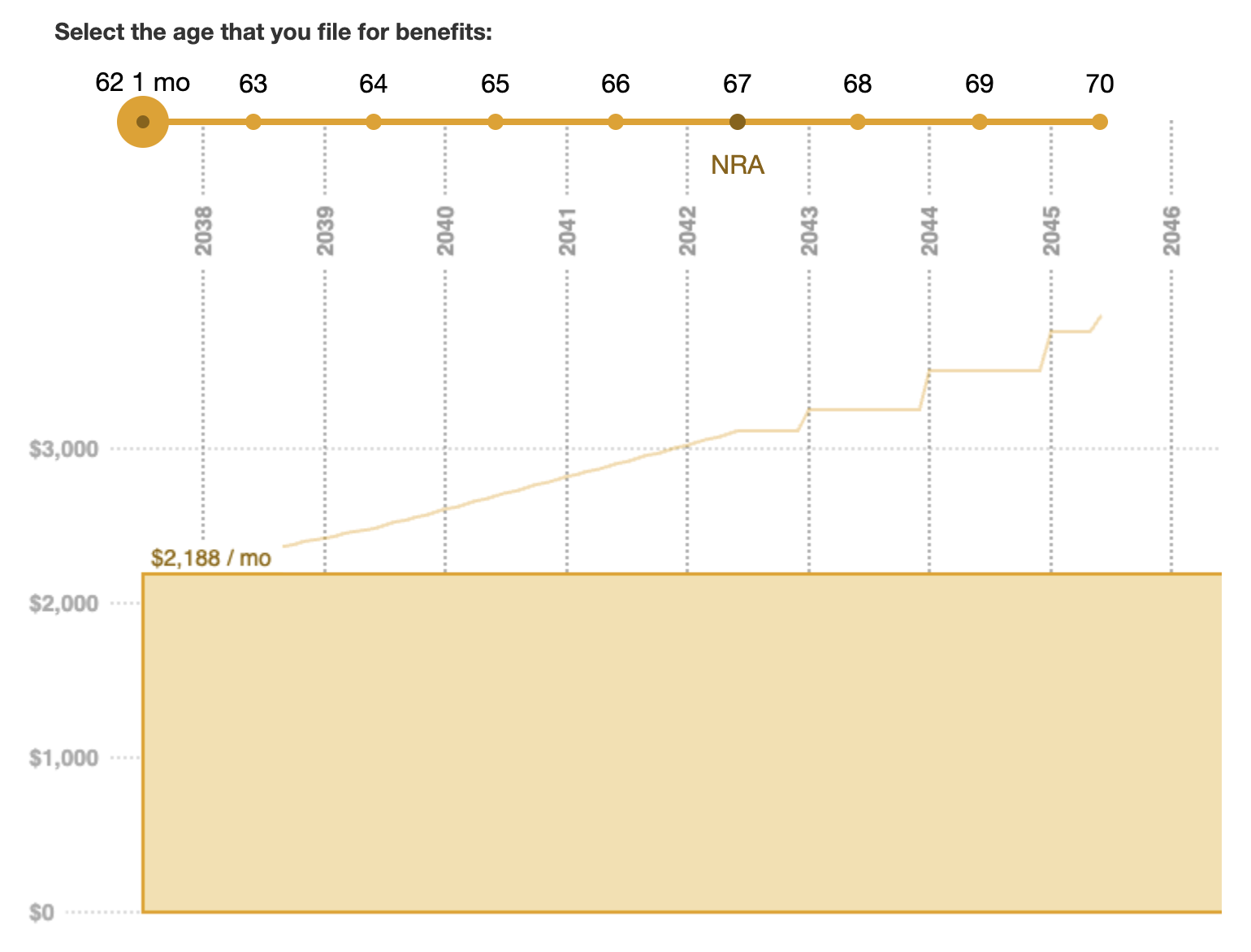

In my case, it would be $2,188 at age 62 and $3,853 at age 70. This assumes I stop working at the moment, simply earlier than turning 50, which was the month I wrote this publish. Word that that is lower than the $2,423 (age 62) and $4,521 (age 70) I’d get if I stored working and paying into Social Safety for 12-20 extra years.

One other cool factor on that little calculator is to see the place you’re on the “bend factors” chart.

When you’re previous the second bend level, like I’m, the bang in your buck on extra Social Safety contributions will not be excellent. Even when I work full-time for 12 extra years and pay six figures extra into Social Safety, my month-to-month profit will solely go up $250 a month.

One other nice free on-line Social Safety useful resource is Mike Piper’s glorious OpenSocialSecurity.com, which is able to truly present some suggestions about when to take Social Safety.

A Few Changes and Assumptions

If I retired now at age 50, my precise profit quantity at age 70 will likely be simply $3,853 per 30 days, or $46,236 per 12 months. Let’s assume half of my profit is greater than Katie’s profit (it is not truly true anymore, however let’s not make this extra sophisticated), in order that’s actually $69,354 per 12 months we’ll begin getting at 70. OK, technically mine will begin coming in earlier than hers, however we will ignore that for simplicity. We’re not quitting work this 12 months both.

Let’s do a hypothetical. As an instance we will work till age 60 and that our mixed profit at age 70 if we do that’s $75,000 per 12 months. THAT is the quantity we have to cowl from age 60 to age 70, and we have to do it in an inflation-adjusted means.

Extra data right here:

5 Causes to Not Give Up on Social Safety

What is the Greatest Age to Take Social Safety?

Find out how to Cowl the Hole

Now, as an instance we have now a $4 million nest egg. If we have been 70 and thought 4.5% was an inexpensive withdrawal fee and we have been getting $75,000 a 12 months from Social Safety, we might spend $4 million x 4.5% = $180,000 + $75,000 = $255,000 per 12 months. That $255,000 must cowl EVERYTHING—together with advisory charges, taxes, and charitable giving, not simply our dwelling bills. However we’re not 70 on this hypothetical instance. We’re 60. And that Social Safety fee is not coming for one more decade. What will we do within the meantime? There are a number of choices, a few of that are higher than others.

#1 Hold It in Money

The primary choice is to take out that cash from the portfolio and put it in money. Since $75,000 per 12 months for 10 years is $750,000, you are taking that cash out of your portfolio and stick it in a high-yield financial savings account or a pleasant cash market fund at Vanguard, Constancy, or Schwab. Yearly, you pull $75,000 out of that account (or each month, you pull $75,000/12 = $6,250 out of the account) and spend it. It’s also possible to spend a part of the remaining nest egg. Since we’re beginning at a youthful age, let’s use a 4% withdrawal fee—4% * ($4,000,000 – $750,000) = $130,000 + $75,000 = $205,000. That is what you’ll be able to spend the 12 months you retire at age 60, with $75,000 popping out of the $750,000 Social Safety alternative fund and the opposite $130,000 popping out of the remaining $3.25 million portfolio.

What’s the issue with this answer? Leaving cash in money for a decade would possibly trigger substantial money drag in your general portfolio returns. To not point out, that is a variety of publicity to excessive inflation. You could possibly withdraw the $75,000 every year plus the earnings from the prior 12 months, however that is not precisely equal to inflation, particularly for the reason that annual earnings would go down because the fund is depleted or as rates of interest change.

#2 Legal responsibility Matching Portfolios

Maybe a extra refined strategy is a legal responsibility matching portfolio. As a substitute of simply sticking all of the Social Safety alternative cash right into a cash market fund, what in the event you divided it into 10 buckets/years and purchased a Certificates of Deposit (CD) or a Treasury bond that matures EXACTLY whenever you want that cash? You set 1/tenth in money, 1/tenth in a one-year CD or Treasury bond, 1/tenth in a two-year CD or Treasury bond, 1/tenth in a three-year CD or Treasury bond, and so forth. Then every year, you get no matter that CD or bond is price PLUS (in the event you’re cautious with the accounting) precisely what it paid out in curiosity over the earlier 12 months(s). Theoretically, you will make extra than simply money charges on this cash, AND the earnings on it should assist make up for inflation through the years.

#3 A TIPS Ladder

The professionals on the market have been chuckling as they learn the final couple of paragraphs.

“What a knucklehead! Why would anybody do that with money, CDs, or nominal Treasuries when TIPS can be found?”

Nice query.

Though not essentially the only means, the academically right approach to do it’s with Treasury Inflation Protected Securities (TIPS). It would be 1/tenth in money, 1/tenth in a one-year TIPS, 1/tenth in a two-year TIPS, 1/tenth in a three-year TIPS, and so forth. You now not want the curiosity to maintain up with inflation; you’re going to get that mechanically with the inflation changes within the TIPS. You could possibly put that curiosity into your nest egg or simply have or not it’s a part of that 4% of the nest egg you are spending every year. You will owe taxes on each the curiosity and the inflation changes (together with some taxes on phantom revenue), however you’ll be able to regulate for that.

A TIPS ladder to me is clearly the easiest way to cope with this challenge, and the much less you will have in your nest egg, the higher an answer it’s for you.

Extra data right here:

A Framework for Considering About Retirement Revenue

Addressing Your Complaints

OK, that appears easy sufficient, proper? However I hear a number of complaints on the market. Let’s handle them instantly.

I Cannot Spend as A lot

The primary one sounds one thing like this: “But when I wait till 70, I can spend $255,000, not simply $205,000. Why would not I do this?”

Do not be foolish. When you wait till age 70 to retire, you’ll be able to most likely spend FAR MORE than $255,000 per 12 months. Not solely do you get to go away that $750,000 within the portfolio, however you get one other 10 years of compounding. Plus, there are one other 10 years of contributing to Social Safety, leading to a better profit than $75,000, and one other 10 years of contributing to your nest egg. Sure, in the event you wait till age 70 to retire, you’ll be able to spend greater than $205,000. The truth is, you can spend greater than $255,000. It would not shock me in the event you might spend greater than $400,000 and even $500,000. That is simply the impact of extra time within the accumulation section.

However there is a value. That value is 10 years of labor. And 10 fewer years in retirement. To make issues worse, all 10 of these years are doubtless go-go years. It is your alternative. As boxing nice George Foreman mentioned, “The query is not at what age I wish to retire; it is at what revenue.”

However That is Sophisticated

One other grievance I hear is that it’s a variety of work to construct a TIPS ladder. Sure, it is a lot simpler to only dump cash right into a TIPS mutual fund or ETF. And even that cash market fund. However I believe the ensures are most likely price it, notably if that Social Safety alternative fund is a big a part of your nest egg (1/3 or extra). There are even web sites that can assist you arrange a TIPS ladder, akin to Tipsladder.com. You do not even must open a clunky TreasuryDirect account; you’ll be able to simply purchase the TIPS at your brokerage at Vanguard, Constancy, or Schwab. You’ll be able to even do it in retirement accounts in order for you, though you will must handle the tax penalties of withdrawals from a tax-deferred account. And if that is all simply too onerous, possibly it’s best to rent a monetary advisor to assist. We now have loads of good monetary planners/asset managers to advocate. They are not free, however they do give good recommendation at a good worth.

I am Going to Ignore Social Safety

Lots of people fear that Social Safety is in political peril. Whereas I don’t share that fear, given its reputation, it is not not possible that advantages can be lowered and even disappear. The drawback with ignoring it, nonetheless, is that it might end in you oversaving, underspending, or working longer than you would favor. I determine that even in the event you’re an excellent pessimist, do not assume Social Safety will not be there; simply low cost it by 25%. Even when Social Safety “runs out of cash” in a decade or so, there’ll nonetheless be sufficient taxes to pay 75% of at the moment promised advantages with none adjustments to this system.

If our hypothetical couple merely takes 4% of that nest egg from age 60, with none kind of Social Safety fund, they will be spending $4,000,000 * 4% = $160,000 as an alternative of the $205,000 I believe they need to be spending. That is 22% much less. And off the highest too, so it is all of the enjoyable stuff.

When you, like most, ought to delay your Social Safety profit to age 70, I hope you now perceive how you can reside/spend/withdraw between your retirement date and age 70.

What do you suppose? When do you intend to retire? When do you intend to say Social Safety? What’s your plan between these dates?

; Inventory Makes Nasdaq High Gainer Listing")

![14 Small Enterprise Apps That Get Stuff Completed [2025 Edition]](https://i0.wp.com/www.dreamhost.com/blog/wp-content/uploads/2023/10/1220_x_628_ogimage_top_smb_apps_2025.webp?w=120&resize=120,86&ssl=1 "14 Small Enterprise Apps That Get Stuff Completed [2025 Edition]")

{kind=link}