During the last 12 months, scholar mortgage packages have modified dramatically. SAVE goes away. The RAP plan is taking its place. And the caps on federal borrowing may have ripple results throughout the medical group. It’s pure to have a way of uneasiness and stress as you look towards the way forward for navigating your scholar loans.

You might be busy and work in a occupation that may really feel extraordinarily gratifying and exhausting on the identical time. Carving out spare time to analysis federal scholar mortgage coverage (134 pages stuffed with legalese) isn’t an pleasant endeavor. Particularly when it appears to alter so usually.

On this publish, I’ll focus on what you could find out about RAP and the coed mortgage program adjustments going into impact on July 1, 2026.

What Occurs to These Presently within the SAVE Program?

After a two-year authorized battle, the Saving On A Invaluable Schooling (SAVE) program is formally coming to an in depth. When SAVE launched in late 2023, it was broadly thought-about the most effective Earnings Pushed Reimbursement (IDR) choice accessible. That’s not the case.

Debtors in SAVE benefited from an curiosity subsidy and fee pause from the summer time of 2024 to the summer time of 2025, just like the COVID pause. Nevertheless, curiosity resumed in August 2025, and the forbearance time in SAVE isn’t initially thought-about eligible as credit score for any federal forgiveness program. If you’re pursuing Public Service Mortgage Forgiveness (PSLF) or IDR forgiveness, these ~two years could not rely towards your whole. There’s a potential treatment to the SAVE forbearance—the PSLF buyback program—but it surely has been largely stalled by the Division of Schooling, with processing occasions presently exceeding three years.

On July 1, 2026, debtors in SAVE may have 90 days to pick a brand new compensation plan. If no plan is chosen, you’ll robotically be moved to plain compensation or the newly created tiered commonplace compensation plan. Tiered commonplace compensation is the brand new default fee program for federal mortgage debtors who borrow later than June 30, 2026. Cost phrases are primarily based on how a lot you owe.

For many white coat buyers, the compensation time period could be over 25 years. This fee program doesn’t qualify for the PSLF program.

Extra data right here:

Serving to a Pre-Med Run the Numbers on Medical College

What IDR Plans Are Accessible Now?

Earnings Pushed Reimbursement (IDR) plans are altering due to the OBBBA invoice handed in 2025. Presently, a borrower can enroll in:

- Previous Earnings Based mostly Reimbursement (IBR): 15% of discretionary earnings for individuals who borrowed pre-July 1, 2014

- New Earnings Based mostly Reimbursement (IBR): 10% of discretionary earnings for individuals who borrowed post-July 1, 2014

- Pay As You Earn (PAYE): 10% of discretionary earnings

- Earnings Contingent Reimbursement (ICR): 20% of discretionary earnings

The most recent IDR plan, referred to as the Reimbursement Help Plan (RAP), is predicted to be accessible in July 2026.

All of those plans qualify for PSLF. Nevertheless, ICR and PAYE will sundown by July 2028. Debtors have to be considering forward about which plan works greatest for his or her scholar mortgage plan.

What Is the Reimbursement Help Plan (RAP)?

Reimbursement Help Plan or RAP is the latest iteration of IDR plans created by OBBBA. RAP has options which are just like the SAVE/REPAYE plans, the place it subsidizes all unpaid curiosity. This ensures that when you make your required fee, your mortgage steadiness won’t ever go greater.

For instance, in case your curiosity grows $1,000 monthly and your required fee in RAP is $300, the unpaid curiosity of $700 is waived ($1,000-$300 = $700). The curiosity subsidy could be very useful to those that are in early profession or in coaching. Usually, the subsidy phases out as earnings will increase once you transfer into observe.

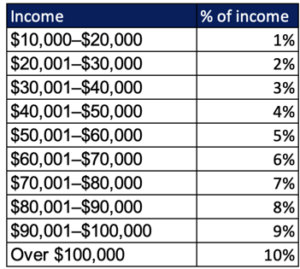

Funds in RAP are calculated as a proportion of Adjusted Gross Earnings.

In case your earnings is beneath $10,000, the minimal fee is $10 monthly and $120 for the 12 months. Not like legacy IDR plans, RAP doesn’t use a federal poverty line deduction. As an alternative, it deducts $50 monthly per youngster (two youngsters = $100 monthly off your fee).

RAP has no fee ceiling, requires direct federal scholar loans, qualifies for PSLF and features a non-public sector forgiveness observe at 30 years (longer than earlier IDRs). Married debtors can file taxes individually to exclude spousal earnings. One distinct characteristic is that funds made whereas on RAP don’t rely towards non-public sector forgiveness eligibility below another Earnings-Pushed Reimbursement (IDR) plans.

Listed below are a couple of examples of month-to-month funds:

- Single resident incomes $60,000 per 12 months: ($60,000 / 12 * 5%) = $250 monthly

- Single resident incomes $60,001 per 12 months: ($60,001 / 12 * 6%) = $300 monthly

Please notice: the RAP plan features a sharp fee cliff, the place even a small improve in AGI can considerably increase your month-to-month fee. Decreasing your AGI by just some {dollars} could assist decrease your required fee and improve your financial savings.

- Single attending incomes $375,000: ($375,000 / 12 * 10%) = $3,125 monthly

- Married attending incomes $375,000 with three youngsters: ($375,000 / 12 * 10%) – 150 = $2,975 monthly (notice the decrease month-to-month fee as a result of family’s three youngsters)

Is RAP the Proper Plan for Me?

RAP is an IDR plan you could make the most of to progress towards PSLF or non-public sector forgiveness, and it’s the solely IDR plan choice when you take a mortgage out later than June 30, 2026. RAP stacks up properly towards Previous IBR and ICR. Nevertheless, it seems to be costlier than New IBR and PAYE.

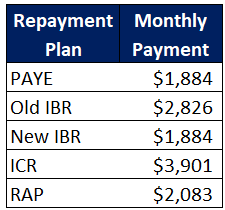

Situation #1 — Excessive Debt Relative to Earnings

Single doctor, $400,000 of scholar loans, pediatrics, incomes $250,000.

RAP is properly beneath Previous IBR and ICR however barely greater than PAYE and New IBR. Let’s now decrease the debt steadiness for this doctor.

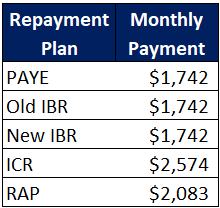

Situation #2 — Decrease Debt Relative to Earnings

Identical doctor incomes $250,000, $150,000 of scholar loans.

RAP’s fee doesn’t change. However you’ll discover PAYE and the IBRs are all decrease as a result of fee cap that kicks in when earnings begins to exceed the mortgage steadiness. The fee cap is a related issue in your scholar mortgage plan if you’re contemplating PSLF and when you’ll earn earnings greater than your scholar mortgage steadiness.

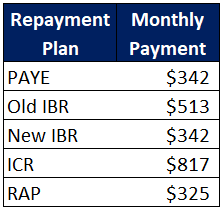

Situation #3 — Trainee

Trainee incomes $65,000 with $150,000 of scholar loans.

At decrease incomes, most plans (aside from ICR) land in the same vary. The important thing differentiator is RAP’s curiosity subsidy, which might maintain your mortgage steadiness from rising.

Selecting the best compensation plan is a crucial step in efficiently managing your scholar loans and staying aligned together with your monetary objectives. In the event you’d like assist figuring out which compensation technique is greatest in your scenario, schedule a time to fulfill with Pupil Mortgage Recommendation in the present day.

Extra data right here:

Want Non-public Pupil Loans? We Can Assist!

Crucial Pupil Mortgage Deadlines Earlier than July 1, 2026

Listed below are probably the most time-sensitive adjustments that might influence your scholar mortgage plan proper now.

Any New Federal Mortgage Issued on July 1, 2026, or Later

That is probably the most underappreciated change within the laws. In the event you take out any federal loans on or after July 1, 2026—even a small one—you change into ineligible for all IDR plans besides RAP.

This is applicable to federal consolidation loans as properly. A direct federal consolidation usually takes 4-8 weeks to course of, and the mortgage date is decided by disbursement, not utility. In the event you’re contemplating a federal direct consolidation proper now, there is a significant probability your mortgage will not disburse till July 1 or later, operating the chance of completely closing off IBR and PAYE as choices.

New Federal Borrowing Caps

New federal borrowing caps college students beginning their program of research after June 2026. Beforehand, knowledgeable or graduate scholar might federally borrow as much as the price of attendance with the appearance of Grad PLUS loans. With Grad PLUS loans discontinued, federal borrowing caps might be:

- $200,000 ($50,000 per 12 months) for medical and dental faculty

- $100,000 ($20,500 per 12 months) for graduate faculty

- $257,500 lifetime cap throughout all federal borrowing

For college students within the class of 2030 and past, non-public borrowing will change into far more widespread to cowl the funding hole. Packages like PSLF might be much less beneficiant with fewer IDR choices and decrease federal balances owed.

In the event you want non-public scholar loans, WCI might help. We have partnered with a number of nice firms that may present nice service and honest phrases (plus, you will get money again and a free WCI course).

† Bonus could embody money rebates and worth of free course. Pupil mortgage debtors who use the WCI hyperlinks might be enrolled in The White Coat Investor’s flagship course, Fireplace Your Monetary Advisor: STUDENT without cost ($99 worth). Debtors should still obtain the wonderful money rebates that WCI has negotiated with lenders. Provide legitimate for mortgage purposes submitted from Could 1, 2026 by October 31, 2026. Free course should be claimed inside 90 days of first mortgage disbursement. To assert free course enrollment, go to https://www.whitecoatinvestor.com/loanbonus.

For brand spanking new non-public scholar loans, we advocate you examine with two or three of those firms and go together with the one providing you the bottom rate of interest and greatest phrases.

What Ought to You Do Proper Now?

The window for a few of you to behave is slender.

- In the event you’re a PSLF candidate nonetheless on SAVE, begin evaluating IBR, PAYE, and RAP now, as you could act quickly.

- In the event you’re in SAVE and never pursuing forgiveness, take into account privately refinancing your scholar loans.

- In the event you’re planning to consolidate now, perceive that your new mortgage will virtually actually disburse on or after July 1, locking you into RAP.

Everybody’s scenario is completely different. Working your individual numbers that think about earnings, household scenario, mortgage steadiness, and employment objectives is the one technique to know which path is greatest for you. If you would like assist working by it, the workforce at Pupil Mortgage Recommendation can stroll you thru the specifics.

What do you assume? Are you planning on enrolling in RAP? Are you continue to in SAVE forbearance? Why or why not?

")

{kind=link}