In the beginning of the yr, I’d normally report how a lot I spent prior to now yr. On this submit, I’ll share my spending within the yr of 2025.

I realized from someplace that we might normally allocate our revenue with this framing:

- My Spending for immediately – These are our present bills.

- My Spending prior to now – These are the repayments on the money owed we owe.

- My Spending sooner or later – These will probably be our financial savings and investments. They’re meant to fulfil a life purpose sooner or later, which would require some cash.

You’ll be able to determine how a lot to spend for immediately, the previous and the long run.

There’s a tradeoff to saving up cash to spend sooner or later, and we should always all acknowledge that. Sadly, some fail to acknowledge the tradeoff, and so they battle with residing life with cash.

Reviewing our spending is a means for us to be extra aware about our spending.

My Previous Annual Earnings Spending Experiences

Updating my spending has develop into a customary replace on an annual foundation. Not everybody could also be . Nonetheless, you is perhaps curiosity in how my spending has developed through the years:

- 2014: $23,798/yr – A assessment of my previous yr’s bills

- 2015: $22,150/yr – How our household’s $22,150 annual bills imply for our monetary safety and monetary independence

- 2016: $26,238/yr – My Annual Expense Report – $26,238/yr and its hyperlink to Monetary Safety and Independence

- 2017: $21,723/yr – Annual Expense Report 2017 – $21,723

- 2018: $19,655/yr – Annual Bills and Monetary Safety Musings

- 2019: $23,186/yr – Spending Report for the Yr

- 2020: $22,464/yr – How I spent $22,464 in 2020

- 2021: $27,680/yr – Annual Bills Report 2021

- 2022: $39,187/yr – Annual Spending in 2022

- 2023: $29,554/yr – Annual Spending in 2023 – Reflection of Spending Consciousness

- 2024: $41,923/yr – Annual Spending in 2024

Within the first 3.5 years, the bills comprised three adults’ spending. The bills have been spent on two adults for the subsequent 4.5 years. The present spend (not included within the listing above) is the spending of 1 particular person (me).

How I Classify My Spending

There have been a number of modifications through the years in how I classify my spending.

I believe if you’re on this path of determining the right way to observe, finances and replicate upon your spending, you’ll have a look at issues in another way. The extra you study, the extra you’ll calibrate the way you have a look at your spending in a means that matches your wants essentially the most.

I revamped my spending final yr after my dad handed away in 2023. The present system suits extra for an individual monitoring their path to Monetary Independence.

I’ve written extensively about how I take into consideration my private cash scenario in My Private Notes part.

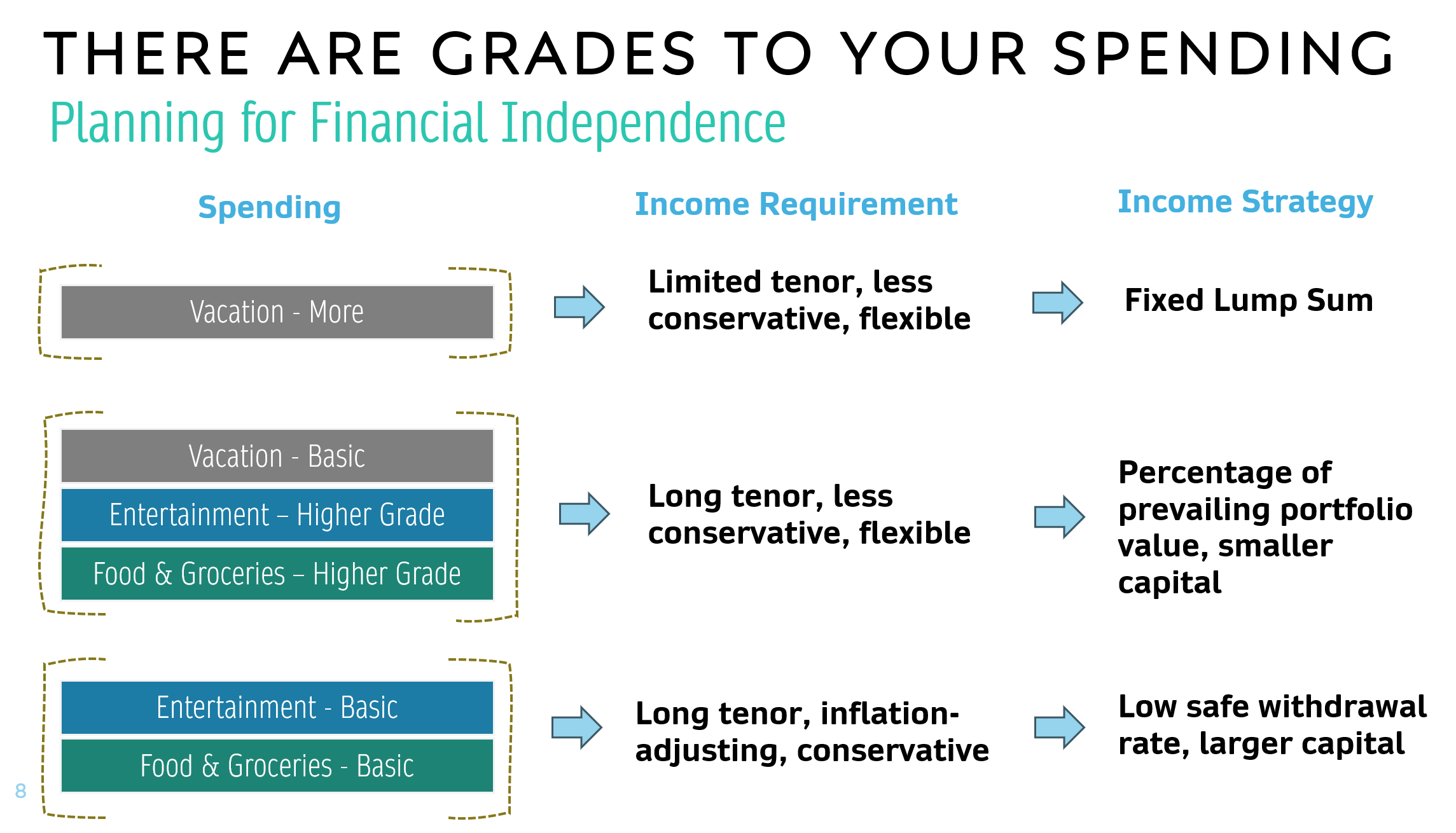

Typically, they’re grouped in order that I can assessment particularly the next areas:

- My most important spending (You’ll be able to examine them in every article). Most rigid and must be most conservative.

- My primary spending. Usually rigid however the timing of spending may be versatile. Largely conservative.

- Spending if I work.

- Spending that may come from portfolio sources.

- Versatile spending. Could be adjusted, scale up or down relying on market situations.

The distinction between every spending group relies on crucial planning traits:

- How versatile or rigid is the revenue/spending wants.

- Does the spending requires inflation-adjustment.

- Whether or not the spending is gong to final perpetually or it ends after sure years.

These crucial traits have an effect on your revenue technique within the following means:

The above is extra like an instance, not how I need to plan out.

The extra rigid, inflation-adjusting or lengthy the spending must be, the extra conservative your revenue technique must be.

Thus, the way you have a look at your spending issues.

Okay allow us to check out 2025’s annual spending.

2025 Spending – $30,768 within the Yr

Right here is how my spending seems:

My whole spending for 2025 comes as much as be $30,768. That is decrease than the $41k final yr and the principle purpose was I donated much less cash in 2025.

You’ll be able to see the month-to-month spending in addition to the whole and common on the backside.

I’ll spend the subsequent few sections to elucidate every group intimately.

Important Rigid Spend – $3,255 within the Yr

The important inflation spend is a class that I’ve my eye on essentially the most. That is the rigid spending that’s most important to life and if this goes up primarily based on inflation, then I’ve to spend this in a means.

I mirrored upon this class and got here up with the next finances for revenue planning:

Up to date 5 Jan 25. Click on to view a bigger desk.

The spending is to be offered by the Daedalus portfolio that I incessantly wrote about, with the newest one right here. You’ll be able to examine why I listing these things and the corresponding quantity on this submit.

Reviewing the spending on this class is to see if this template nonetheless make sense.

My spending in 2024 is about $1000 greater than in 2023. This time the spending dropped again to nearer to 2023 stage. The most important distinction is as a result of spending in Utilities, Conservancy & Important Replacements, which noticed a discount from $2,239 to $1,117.

For readability the widespread objects that goes into listed here are:

- Property Tax – not paid this yr however possible paid this month. My property tax in FY2026 is $212 [last year is $172 so that is a 23% increase!]

- Broadband – $7 month-to-month this yr

- Private Cellular Subscription – $15 month-to-month this yr

- City Council Expenses – $89 month-to-month this yr (with out subsidy) [this is higher. Last year was $78]

- Utilities (Water, Fuel, Electrical energy) – $0 month-to-month common [100% offset by U-save

- Laptop Replacement

- Mobile Phone Replacement

- Refrigerator Replacement

- Toiletries

I probably provision a budget of $3,364 annually for this and so spending $1,117 is still within the limit.

This year I did not replace the fridge, mobile phone or laptop/computer so this explains the lower spending. I do suspect I might replace the computer and mobile phone so the spending is higher.

I saved up $200-$240 annually for each of these replacement, whether I spend in the year or not. This is a discipline way of provisioning for spending that would eventually happen.

My food spending of a total of $1,063 is low compare to about $4,320 because of a few reasons:

- CDC Voucher subsidizing grocery and food spend.

- Meal prepping. You can read about my meal prep here.

- I would usually eat 2 meals a day.

There are those who say the cost and time is not worth it but with the basic food cost approaching $5-6 per meal, food prepping becomes more worth it. Still I do set my budget as $6 per meal for 2 meals a day. With meal prep, I do average $6 in food cost a day. But as you can see the food cost is even lower.

As a worker, the transport cost averages $90 a month but if I am not working, I do think this will go down dramatically.

I did not pay any utilities this year due to U-Save vouchers.

Lastly, I have 2.5 months of Town Council fee rebate in the year.

My essential inflexible spend of $3,255 is lower than the $10,244 plan for in 2023.

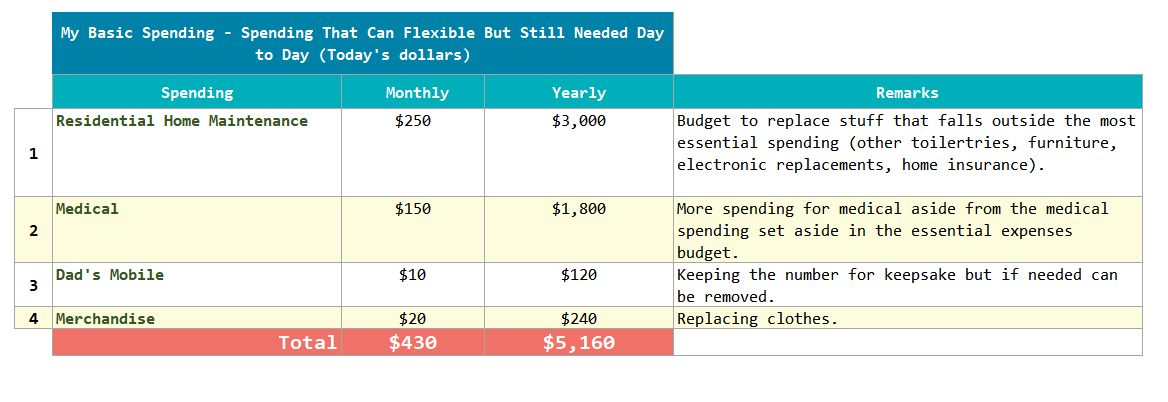

Basic Inflexible Spend – $1,952 for the Year

The Essential Inflexible Spend are the spending that allows a person to run for a long time at the minimum.

However, the reality is that you would have to provide for more in the house. Things break down in the home and you want to improve things over time. You also want to provide for more medical needs. You will have to spend on basic inflexible spend but if market conditions are not so good, you can shift when you spend it. But you would ultimately have to spend and cannot cut down much.

I wrote about provisioning $5,160 a year for things like this:

You can read more about this in this post here. This spending will come from Daedalus income portfolio as well.

I spent $1,952 in 2025 and this is not too different than the $2,266 spend in 2024. This is still lower than the $5,160 provision in the year.

Whatever is not spent here (about $3,000 here) is accumulated annually. This is especially so for the excess $1000 in residential home maintenance which will eventually be needed to replace something pretty necessary such as washing machine, painting, 10-15-yearly renovations.

You might also notice that the spending is pretty lumpy and if you are less seasoned with budgeting, you might struggle to make sense of it.

Flexible Spend – $15,928 in the Year

Flexible spend is what you would call your Discretionary spending. The kind of spending that makes life meaningful. This is also the spending that you think you can be flexible about.

Why does this matter in your income planning?

If you are really flexible with this, then if the portfolio is not doing well, then you can cut your spending. You have to deeply reflect if you can cut this.

Aside from income tax, flexible spending is where I spend 50% of my annual spend.

Last year, I spend $25,734 so this is also a reversion back to my 2023 spending.

I contributed $0 to nursing home this year. We got higher subsidies for my grandmother, who is in a nursing home so my aunt told us this is less needed. Still, I think we should eventually plan for a day where we won’t get so much subsidy so I continue to contribute.

Premium meals are the discretionary meals I spend out celebrating events, treating friends and family. If I am doing well, there will be more and if not, this will be more controlled. This amount is not too different from last year. I don’t control my premium meals and this is very volatile but they somehow don’t change much.

I don’t budget a fixed amount for premium meals but just spend them. If I meet or decide to go out more to have a good time, this will increase and vice versa. 2025’s premium meals is not too different from 2024’s.

The fun and hobby spending is lump under Entertainment and Hobbies. This is where my nonsense spending is and this went up like 100% this year. Providend Gifts are the spending that happen accidentally or intentionally because of where I work. This year’s spending is just slightly lower than last year.

You will gain more insight about my flexible spending if you go to my personal notes section and take a glimpse at My Spending Log under How I think about other areas of my current recurring expenses.

I gifted 50% less to people. The amount that I spend at Providend went up by 30%. Gokoku and Baker’s Bench probably amount for a mass majority of that lol.

I spent less on vacation this year as well.

The Rest of My Spending

The rest of my spending includes:

- Income Tax under Work

- Insurance Premiums under Funded by Net Wealth

My income tax is a function of work and blog income. If there are inflows, this is a necessary outflow. Don’t have to think about it so much except to have enough liquidity to pay for it.

Despite Investment Moats revenue falling strangely I seem to be paying less.

I have set aside capital to pay for future insurance premiums so that won’t come from the salary. You can read about it at Cutting My F.I. Capital Needs for Insurance Premiums from $131,366 to $58,132 by Prepaying for It.

Insurance premiums are up.

I suspect that I have to account for my hospital and surgical insurance plans better to attribute part of that as what I provision in my Essential Inflexible Spend.

End of the Year Spending Reflection

There ain’t a lot to learn from study how I eat, move about and spend on the things that keep the household going after doing this for the past decade.

While tracking your spending is important, review and reflection is where the value is.

How you frame or group your spending is critical because it simplifies the kind of planning you wish to do.

Not everyone appreciates the nuance part of it but I am glad some of my friends do.

I profiled how a Telegram group member who decide to shift his budgeting grouping in 2024’s review. This year I want to share my friend CentsofIndpendence’s slight shift in framing:

She and I had ongoing conversations about dealing with how she spends her money annually and financial independence planning [Coast FI, and Full FI]. I are inclined to assume you’d try however keep on with a sure framework in case you perceive and discover worth with it.

In the identical vein, she teams her spending primarily based on spending which can be important which can be extra mounted, extra variable, the discretionary one (FUN), and in addition some spending that may go away if life modifications (Work), and time restricted (mortgage).

In 2025, she thought extra about

- the right way to really feel protected and safe along with her revenue, if she decides to exchange her tutoring revenue with one thing else.

- contemplating the right way to match her mortgage funds, which is a restricted time spending, with the property that she has however on a money movement foundation.

All these would possibly sound just a little detailed for a few of you, however some would additionally ponder about these items.

By grouping her spending primarily based on how important/rigid, restricted time/perpetual, it permits her to hyperlink higher to her property as she will break up her property to sub-portfolios to plan conservative funding.

You’ll be able to learn extra at her Instagram:

There are not any proper or improper strategy to plan, or to trace.

And you might not need to hassle with it.

Nonetheless, if you need higher management of your life and the way cash service it, in some unspecified time in the future it’s essential to have a framework both mentally or have somebody take care of it.

Our finances ought to replicate our values and the way we want to stay our life. The finances would possibly replicate concern, conservatism or abundance.

How I Monitor and Price range My Spending

I exploit a free and opensource self-hosted YNAB-style Envelope budgeting system name Precise Price range.

You’ll be able to learn up about ActualBudget right here.

A YNAB-style envelope system permits us to see how a lot cash that’s collected in an envelope over time. That is one thing lots of different system battle to design.

ActualBudget’s reporting have improved by leaps and sure.

I used to be in a position to provide you with this text with the assistance of the studies and the transaction filtering.

I created a collection of YouTube video of ActualBudget together with the right way to set up, setup your budgeting system.

You’ll be able to view the playlist right here.

However I additionally discover the great factor about it being free is that there are increasingly more YouTube movies on Precise Price range. That is nice as a result of it creates a bit community impact.

Month-to-month Spending Put up

From mid of 2025, I determine to begin posting my month-to-month spending on Funding Moats. You would possibly catch a more moderen month-to-month submit like this.

You’ll be able to see all of the bizarre stuff I spend cash on.

Often, I don’t publish my month-to-month spending right here however if you’re I do publish them on my Instagram. In case you are you’ll be able to test it out.

If you wish to commerce these shares I discussed, you’ll be able to open an account with Interactive Brokers. Interactive Brokers is the main low-cost and environment friendly dealer I exploit and belief to speculate & commerce my holdings in Singapore, america, London Inventory Trade and Hong Kong Inventory Trade. They permit you to commerce shares, ETFs, choices, futures, foreign exchange, bonds and funds worldwide from a single built-in account.

You’ll be able to learn extra about my ideas about Interactive Brokers in this Interactive Brokers Deep Dive Sequence, beginning with the right way to create & fund your Interactive Brokers account simply.

Kyith is the Proprietor and Sole Author behind Funding Moats. Readers tune in to Funding Moats to study and construct stronger, firmer wealth foundations, the right way to have a Passive funding technique, know extra about investing in REITs and the nuts and bolts of Energetic Investing.

Readers additionally comply with Kyith to learn to plan effectively for Monetary Safety and Monetary Independence.

Kyith labored as an IT operations engineer from 2004 to 2019. At the moment, he works as a Senior Options Specialist in Insurance coverage Begin-up Havend. All opinions on Funding Moats are his personal and doesn’t characterize the views of Providend.

You’ll be able to view Kyith’s present portfolio right here, which makes use of his Free Google Inventory Portfolio Tracker.

His funding dealer of alternative is Interactive Brokers, which permits him to put money into securities from totally different exchanges all around the world, at very low fee charges, with out custodian charges, close to spot foreign money charges.

You’ll be able to learn extra about Kyith right here.

Positive aspects on Information Heart Information")

")

{kind=link}