A money stability plan is an incredible car that permits high-income medical doctors to build up important tax-deferred belongings over a comparatively quick time period.

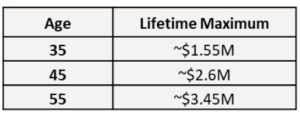

In 2025, a lifetime most for a 58-year-old is about $4 million, and this may be gathered over a 10-year interval. There are massive benefits to maximizing tax-deferred account contributions for these within the highest tax brackets. It may be demonstrated (see chart under) that, over a 10-year interval, a money stability plan may be very advantageous vs. a taxable account for these within the highest tax brackets. It could take a mean taxable account fee of return of between 10%-12% to only break even with a money stability plan with an curiosity crediting fee (ICR) of 4% (assuming 37% federal and 0%-10% state brackets). Furthermore, there’s a Roth conversion technique that’s out there for these with excessive tax-deferred account balances, sometimes carried out in retirement, that may considerably lower the tax legal responsibility whereas permitting large Roth account development, so having a big tax-deferred bucket is a bonus reasonably than a drawback vs. having all the cash in a taxable account.

The chart exhibits the break-even return calculation of a money stability plan vs. taxable, with a beneficiant assumption that no dividend/capital positive aspects taxes had been paid within the taxable portfolio. With taxes included, the break-even return could possibly be as excessive as 12%. The annual value distinction accounts for the truth that extra cash from money move was used to pay taxes. That would have been invested as a substitute. Equivalent outcomes will be obtained if the taxable contribution quantity is decreased by the quantity paid in taxes. This illustration assumes no NHCE workers, which is true for group practices the place solely companions are employed. For practices with workers, the evaluation might want to embody the additional employer contribution value.

Whereas a money stability is usually a nice plan for the suitable sort of medical or dental apply, there are a number of points that may doubtlessly make it a dangerous and expensive funding. Probably the most widespread situations in a bunch apply is when a accomplice leaves or retires. The whole lot is okay till they wish to take a distribution. Issues can go sideways when a distribution is requested if the worth of plan belongings has fallen considerably. Even when the plan was absolutely funded when the accomplice’s distribution account worth was calculated, if at precise distribution time the worth of plan belongings falls, absent any planning, the plan sponsor could be answerable for making up the shortfall. Because of this the departing participant will get 100% of their account worth, and the plan sponsor (all of the companions) will contribute cash to the plan to make up the losses. Whereas this example will be utterly averted, the apply management ought to have the information to ensure this doesn’t occur with some prior planning.

One other scenario is an underfunded or an overfunded plan resulting from portfolio volatility. When a plan is underfunded, the companions should make up the distinction within the yr when the underfunding happens. Whereas this could typically be pushed into the subsequent plan yr, it isn’t advisable because of the potential snowballing impact. An overfunded plan has an reverse concern—if the return is greater than the crediting fee, the federal government, at plan termination, will find yourself taking 90% or extra of the overfunded quantity within the type of excise taxes. So, underneath some circumstances, overfunding might grow to be a difficulty as nicely.

It is rather widespread to see money stability plan investments managed improperly. It’s pretty widespread to see actively managed portfolios with a number of turnover consisting of a number of actively managed funds with excessive expense ratios or, worse, particular person shares and even illiquid investments which can be exhausting to redeem rapidly. For many money stability plans, there may be an extra Belongings Underneath Administration (AUM) price utilized to the plan belongings. It’s also fairly widespread that the plan adviser will not be an ERISA 3(38) fiduciary, so all of the legal responsibility for funding efficiency falls on the shoulders of the plan sponsor. Most such advisers will not be very educated about money stability plans and tips on how to correctly assemble the suitable sort of portfolios which can be acceptable for such plans. As a result of the majority of advisers cost AUM, some could even attempt to oppose cheap methods that cut back this AUM (and therefore their charges), comparable to “terminate and restart” (mentioned under) which is usually a useful gizmo to reduce plan danger resulting from portfolio volatility.

As a result of complexity of money stability plans, there’s a common lack of information of the interior workings of those plans by the plan sponsors who undertake them and by their advisers. This will result in hostile situations that may simply be averted with the suitable sort of planning. On this article, we’ll overview the money stability plan fundamentals and talk about methods during which the danger to the apply will be minimized by implementing superior planning methods—together with tips on how to deal with distributions to departing companions when there’s a shortfall, acceptable funding administration to align with liabilities, and various plan design issues (comparable to precise fee of return vs. fastened fee of return, PBGC vs. non-PBGC plan design, in-service distributions and “terminate and restart” technique).

Money Stability Plan Overview

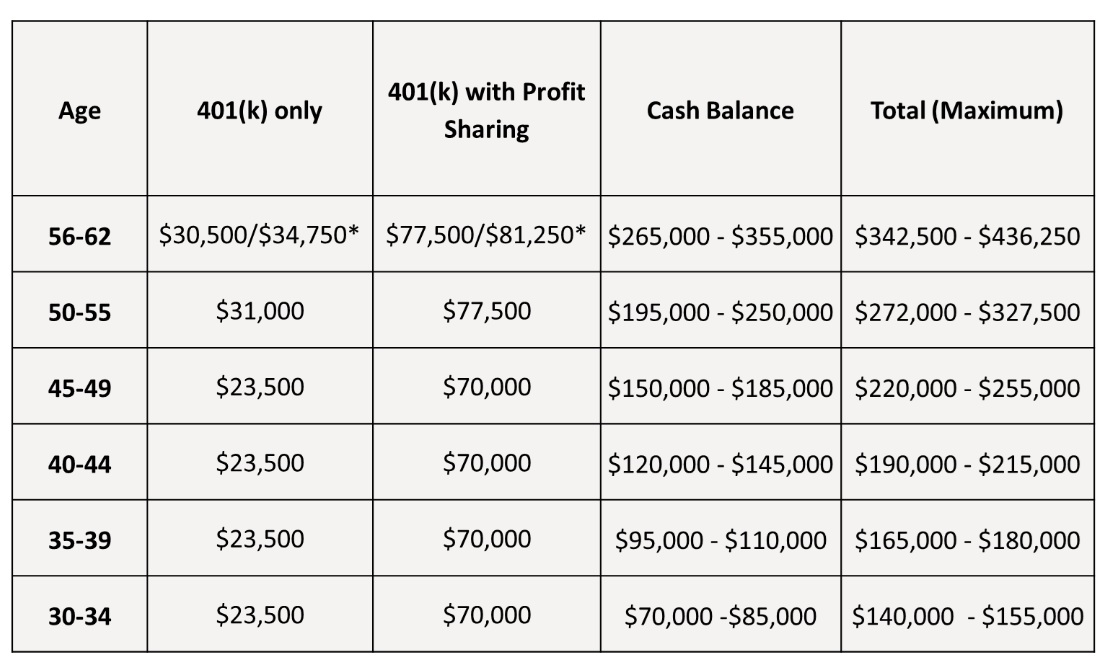

Money stability plan contribution ranges, assuming most profit-sharing contributions [2025].

First, some key information on how a money stability plan works. A money stability plan permits house owners/companions to build up a lump sum based mostly on their age and compensation. Companions/house owners can specify their annual contribution quantity based mostly on their age and compensation (see chart above). Companion contribution is calculated utilizing age and W-2, and it assumes a most plan period of 10 years. On the finish of the 10-year interval, assuming that they’ve made most doable contributions, every accomplice will obtain a lump sum referred to as their ‘lifetime most’ (see chart under). If the plan stays open after a accomplice has reached their lifetime most, they will solely get the crediting fee, and no additional contributions could be doable.

Over time, your plan will probably be amended to permit for inflation changes, which implies your ultimate lump sum (and subsequent contributions) will probably be elevated over the course of 10 years. Most of these changes occur about as soon as each three years.

Money stability plans have a hypothetical crediting fee (aka ICR or Curiosity Crediting Price), and participant belongings are credited this fee annually. Money stability plans are valued annually to be 100% funded. If the plan return is decrease than ICR, the plan sponsor will make an additional contribution into the plan, and if the return is greater than ICR, the plan sponsor’s contribution will probably be decrease. Generally, over 90% of the entire plan contribution will probably be given to the companions/house owners, so a small underfunding is okay, as a lot of the further contribution is given by the companions to themselves.

A money stability plan, in the beginning, is a option to decrease your tax legal responsibility, and it shouldn’t be handled as an funding account. One factor to bear in mind is that it doesn’t matter what the return on the belongings is in a money stability plan. It is because your lump sum distribution quantity doesn’t rely on asset efficiency. It solely will depend on age and W-2, and if one maximizes their contribution, this quantity will probably be fastened. If the funding return is decrease, your contribution will improve, and whether it is greater, it is going to go down. After 10 years, the lump sum would be the identical whether or not the belongings returned 3% or 10%. Within the case of a ten% return, this may considerably lower the quantity that may be contributed on an annual foundation (or it will possibly result in eventual overfunding of the plan).

Provided that we anticipate to pay out 100% of the belongings to departing members and on plan termination, having both not sufficient return (underfunding) or an excessive amount of return (overfunding) is likely one of the greatest issues that we should deal with. Within the case of underfunding, we run into the problem of constructing distributions to retired/terminated members who should obtain 100% of their account worth (as of the final valuation accomplished), so if the account worth fell under that, the plan sponsor should make up the shortfall. Within the case of overfunding, there are methods to make use of up the additional return up to a degree, and this may require maintaining the money stability plan open. A few of this cash will be moved to a 401(okay), however no tax deduction will be claimed. And if the overfunding is excessive, it would take a very long time to make use of up this cash if all members have already maxed out their CB contributions.

In brief, having a fee of return greater than the plan’s crediting fee can result in points, and if the plan have to be terminated for no matter purpose, there’s a risk that any extra could be taxed by the federal government at a fee of 90% or greater.

Extra info right here:

Money Stability Plans: One other Retirement Account for Professionals

High 10 Money Stability Plan Errors to Keep away from

Departing Companions with Giant Balances

One of many greatest points group money stability plans will expertise is when companions with massive account balances depart the group and request distributions from the money stability plan. Valuation is finished for the prior yr, so if, between Dec. 31 and the distribution time, the worth of plan belongings went down, the companions will nonetheless get 100% of their belongings as of Dec. 31. The plan sponsor then must make up the distinction, except prior preparations had been made. This usually comes as a shock for each the plan sponsor and companions, but it surely shouldn’t be. This can be a commonplace function of money stability plans. The one time it turns into a difficulty is when the belongings of the companions who’re leaving are important ($500,000 or bigger). Because of this if a accomplice is leaving with $500,000, and the distinction between the Dec. 31 valuation and the distribution time is, say, 10%, the plan is accountable for $50,000 because the accomplice will obtain all the $500,000 on distribution. If the distributed quantity is greater, say $1 million, we could also be taking a look at numbers within the $100,000 ballpark.

To keep away from one of these scenario, a number of steps have to be taken. Step one is to coach the companions and the plan sponsor on one of these state of affairs. The second step is to take motion to implement an method to mitigate this. A technique to try this is to incorporate particular clauses within the partnership settlement, the place every accomplice is obligated to make up their very own portion of the shortfall to the plan. The partnership settlement will be amended to offer for an extra contribution to be made by departing companions when essential to fund the plan for distributions. The third step is to make sure that when the accomplice leaves the apply, there may be cash left over to cowl any shortfall, whether or not by way of a plan contribution or exterior of the plan. The small print of this association will be labored out by each ERISA and apply attorneys.

Whereas there could also be issues relating to ERISA vs. contract regulation enforcement, it’s higher to be proactive than find yourself holding the bag when no planning is finished to mitigate one of these state of affairs.

Minimizing the Threat to Your Plan

Teams can take extra steps to reduce the danger to their plan and to make sure that the plan is managed prudently, and we’ll think about every of those factors in additional element under:

- Implement a low volatility portfolio.

- Take into account an precise fee of return (ARR) plan, the place solely shortfalls under 0% are made up at distribution (so in case your plan has a excessive crediting fee, the distinction will be decrease in the event you solely make up the loss as much as what you’ve contributed, lower than the crediting fee). The sort of plan design will not be for each apply, however this could additionally mitigate the requirement to make up the shortfall as much as the crediting fee by remaining companions. Not everybody needs to extend contributions throughout down years, and this could doubtlessly deal with that concern.

- Take into account terminating and restarting your money stability plan if it has been round for a minimum of 7-10 years.

- Amend the plan doc to permit for in-service distributions to members beginning at age 59 and ½.

Portfolio and Funding Volatility Defined

The underlying explanation for most of the points confronted by the practices that undertake a money stability plan is portfolio volatility. There’s a common misunderstanding of how this impacts many points of the plan’s operation, together with funding volatility, distributions to companions, and plan termination. Greater volatility merely means a bigger vary of anticipated plan returns. Very often, the Curiosity Crediting Price (ICR) for a lot of older money stability plans is 5%, and lots of advisory corporations construct stock-heavy portfolios attempting to match the ICR with returns. This comes from the mistaken perception that portfolios ought to be constructed to “match” or “beat” the ICR.

In money stability plans, that’s not how issues work. Volatility can simply lead to an underfunded or an overfunded plan, and this could adversely influence the plan’s operation, together with forcing the plan to make up losses whereas offering distributions to departing companions (if preparations haven’t been made to mitigate this) and doubtlessly having points with plan termination. Money stability plans for smaller practices sometimes final for 10 years, however for bigger practices, they will final rather a lot longer than that if there are sufficient companions who can nonetheless take part (and if there may be a minimum of 40% participation, which is a key requirement for any money stability plan).

Nonetheless, there are a lot of situations underneath which money stability plans have to be terminated comparatively rapidly with out a lot discover. Mergers, dissolutions, and hostile enterprise situations are a number of the causes money stability plans will be terminated early, which may end up in asset liquidation underneath doubtlessly unfavorable circumstances. Underfunding would result in doubtlessly massive contributions, whereas overfunding can result in excise taxes on any positive aspects above the ICR (particularly if there is no such thing as a capability to make use of up the positive aspects over time). All these points are brought on by extreme and unpredictable volatility. Thus, avoiding volatility as a lot as doable is the secret right here, as this may reduce the danger to the plan.

Shares introduce further volatility, which signifies that if we wish to reduce our danger, shares ought to be averted in any respect value. What about matching the ICR, you may ask? Even when we actually tried, there is no such thing as a approach anybody can match an ICR with out utilizing illiquid and/or complicated funding merchandise. Common returns even for the least unstable portfolios of bond funds can have a selection across the ICR that we can’t management. What we will management is how massive this unfold is, and whereas we will try to reduce it, we can’t assure that our common return will probably be precisely ICR. That, nevertheless, will not be a difficulty if we have now the bottom doable volatility. Having some underfunding or some overfunding is appropriate whether it is comparatively small and doesn’t trigger the identical points as massive underfunding and overfunding (a number of share factors vs. 10%+, for instance).

Funding volatility occurs when variations between portfolio returns and ICR necessitate further contributions (or diminish your out there contribution quantity), and that is amplified as particular person account balances attain $500,000 and above. In case your account stability is $1 million, a 5% underperformance relative to the ICR will lead to an additional $50,000 contribution, whereas a 5% outperformance relative to ICR will diminish one’s potential contribution quantity by $50,000. A better ICR will lead to a bigger funding volatility, and so will a excessive volatility funding portfolio. Funding volatility is particularly a difficulty when there may be underperformance.

A plan will be frozen if the group doesn’t wish to make up the shortfall in the identical yr, but when underperformance continues, this could snowball into a bigger shortfall. Funding volatility is a big concern that have to be addressed completely in order that it doesn’t grow to be an issue later as soon as the belongings within the plan develop.

Extra info right here:

Evaluating 14 Sorts of Retirement Accounts

Portfolio Design to Reduce Funding Volatility

Now that we have now established that volatility will not be our pal and that we’re not rewarded for beating the crediting fee, particularly when the draw back may be very probably, the query is: what ought to our portfolio seem like?

Listed here are the design constraints for a perfect money stability plan portfolio:

- Whereas a typical small apply money stability plan has a hypothetical 10-year horizon, one of these plan is usually terminated with little or no discover.

- We should always spend money on such a approach as to reduce drawdowns, and we should always try to insulate our portfolio as a lot as doable from market fluctuations.

- Our portfolio ought to present a constant return that’s comparatively regular.

- Drastic adjustments in rates of interest mustn’t have an effect on our portfolio in a serious approach.

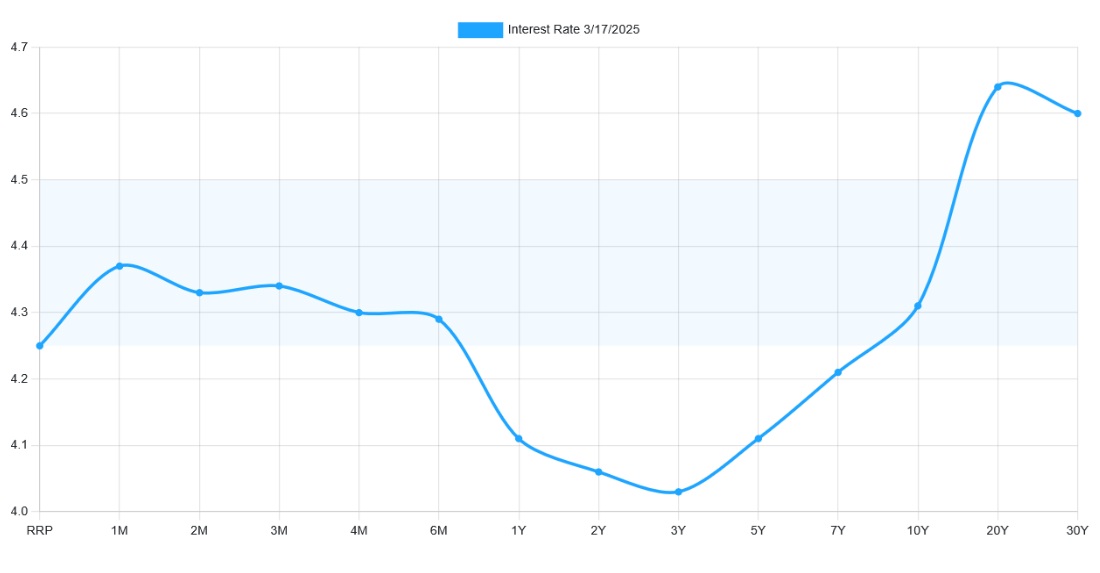

It’s fairly clear that, with these constraints, shares won’t add any worth to this portfolio as a result of they may make it much less predictable and extra unstable. Bonds must also be chosen rigorously. Length is a measure of bond danger, and bonds with greater period misplaced 10%+ in 2022 when rates of interest rose rapidly. From the chart above, it’s apparent that, a minimum of in 2025 (if the yield curve stays the identical), we will keep on with the shorter finish of the yield curve with out having to take further danger to get extra yield.

One massive danger for any portfolio that has bonds in it’s the rate of interest danger. Thus, a laddered bond portfolio ought to be designed to face up to massive adjustments in rates of interest. When rates of interest go down, the value of bonds goes up, and when bond costs fall resulting from rates of interest going up (which is what occurred in 2022), we anticipate our portfolio to fall rather a lot lower than the entire bond market index as a result of we don’t have a lot publicity to the longer maturities or company bonds. Nonetheless, such a portfolio can drop as a lot as 3%-4% in a comparatively quick time period (in comparison with 10%+ for a lot of different bonds, together with the entire bond market index).

As a result of volatility skilled in 2022, that is one of the best method, given how quick our horizon is. However, your 401(okay) plan could possibly be invested as riskily as you want to, provided that the money stability plan is all bonds. You possibly can think about your money stability plan as your bond allocation, and you’ll construct up your 401(okay) and taxable allocation to be extra aggressive. This fashion, we get one of the best of all worlds, and also you get your money stability plan working as a tax shelter reasonably than as a speculative funding that may make your life tougher than it needs to be. After about 10 years, you can transfer the money stability plan funding right into a 401(okay) plan and rebalance right into a extra aggressive allocation.

Mounted vs. Variable/Precise Price Of Return (ARR)

Up to now, we have now mentioned a set crediting fee. Whereas a set fee of return plan has a crediting fee between 3%-5% (with the speed sometimes being set between 3%-4%), some may wish to have the next fee of return than that. Others may wish to lower the funding volatility and deal with the problems associated to paying out terminated members when the plan portfolio has a loss. There’s one other sort of crediting fee referred to as precise fee of return, aka market return, the place the funding return will be variable. There’s a number of misunderstanding about one of these plan.

Listed here are some key factors relating to the precise fee of return plan.

- The annual curiosity crediting fee will probably be an precise fee of return as much as 5%. There are some plans with charges as excessive as 6%, however these are very uncommon.

- When the return is lower than 5%, will probably be allotted in proportion to the beginning account balances.

- A participant’s distribution can’t be lower than the sum of the entire allocations, and that is solely utilized at distribution.

- The one time the plan could be thought-about underfunded could be when the cumulative return is unfavorable and also you want to pay out a participant.

- There will probably be solely a single annual valuation and returns will probably be allotted on the finish of the yr, so the belongings don’t accrue credit till the top of the yr valuation (vs. a set crediting fee the place curiosity is accrued all year long). Because of this any distributions will probably be taken at the start of the yr, and never all year long (as is feasible in a set fee of return CB plan).

- If the return exceeds 5%, the overfunded quantity can be utilized to offset future contributions. If the overfunding turns into sizable, the plan will be amended to allocate the surplus among the many companions. With massive overfunding, we’re nonetheless in the identical area as with fastened fee plans—an excessive amount of of an overfunding in a terminating money stability plan that’s maxed out will result in potential excise tax points.

At first look, one of these plan permits for the next fee of return (sometimes capped at 5%), and members don’t have to make further contributions into the plan even with a return under 0%. Nonetheless, when distributions are made, members merely get the sum of their credit/contributions at no matter return the plan portfolio produced. This eliminates the funding volatility (as the one time the plan is underfunded is when the return goes under zero) and this additionally avoids the problem the place a participant will get 100% of their account worth and should make themselves entire if the distribution quantity is lower than the valuation quantity.

Some may suppose one of these plan would permit for greater risk-taking to doubtlessly get the next fee of return. The truth is, it’s the reverse: given the upper uncertainty, we ought to be much more cautious since taking an excessive amount of danger can lead to a decrease pot of cash after 10 years. Whereas we will doubtlessly get as a lot as 5% return if we’re fortunate, we will even have a unfavorable return if we’re unfortunate. If a higher-risk portfolio is used, volatility will go up, and we’d find yourself with rather a lot much less cash than with a set fee of return that makes use of a low volatility bond portfolio.

Ten years will not be a very long-term investing horizon, so something can occur. It additionally seems that resulting from testing complexities, precise fee of return works solely when companions/house owners are the one ones collaborating in a money stability plan. Given all of the above, when offered with the fastened vs. variable choices, many plan sponsors go for a decrease fastened ICR vs. the next variable one.

In-Service Distributions

One other good option to decrease the danger of your money stability plan is to permit in-service distributions to members who’re a minimum of 59 ½. Usually, any participant who’s 62 years previous can request in-service distribution of their belongings right into a 401(okay) plan. This can be a good thought as a result of many older members will greater than probably have bigger account balances, so if they will transfer their cash to their 401(okay) plan or an IRA, this may hold the belongings within the plan from rising too quickly.

Another choice is to permit in-service distributions at age 59 ½. This often requires the plan to be funded at 110%, however this isn’t a difficulty, as actuaries have other ways during which to reach at that quantity with out requiring a lot, if any, extra cash to be contributed. Most of these distributions are sometimes allowed to be made every year, and the logistics could be offered to the plan sponsor by the actuaries.

PBGC vs. Non-PBGC Money Stability Plans

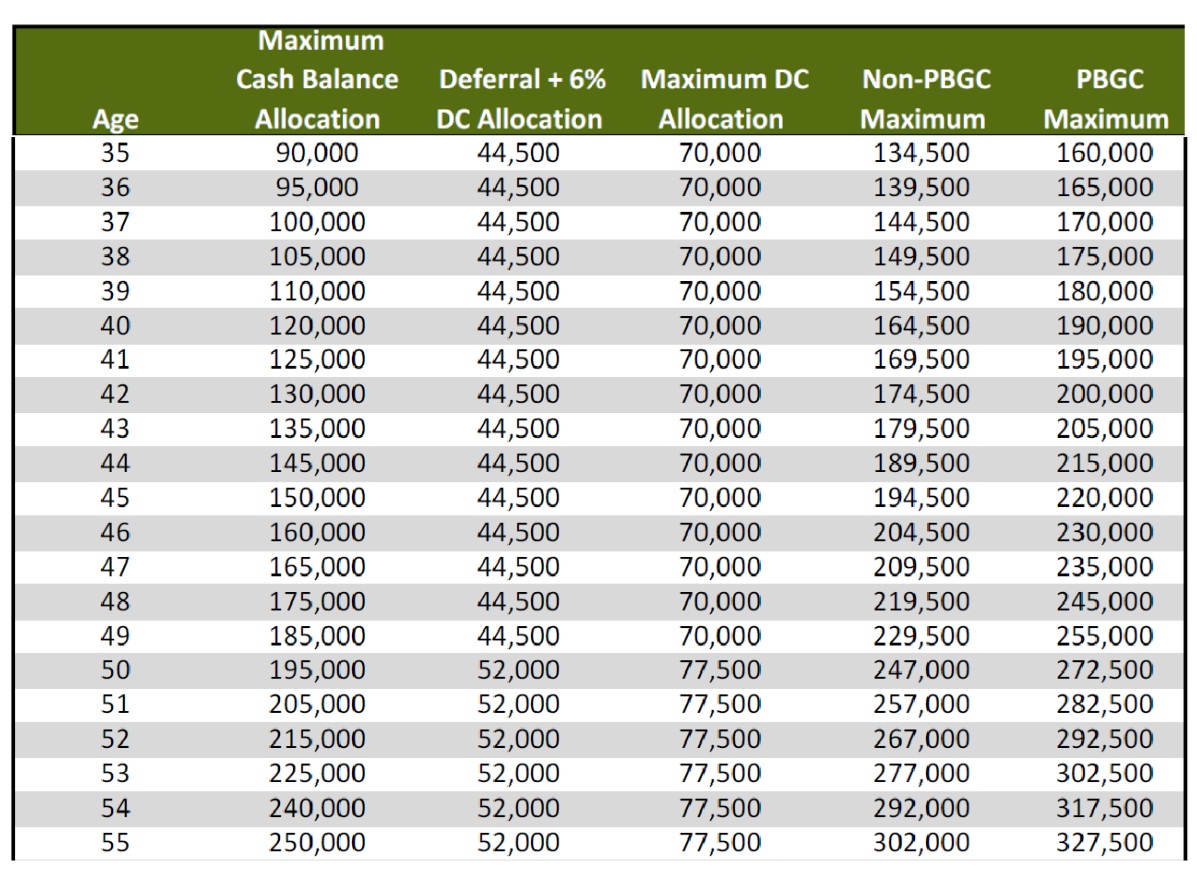

PBGC vs. non-PBGC contributions (2024). The primary distinction is the 6% profit-sharing limitation in a non-PBGC coated money stability plan.

This can be a matter that all the time comes up with smaller practices—particularly when the apply has fewer than 25 companions and workers or if the potential money stability plan can have fewer than 25 members even when the apply is bigger. As soon as there are greater than 25 members within the plan, it’s coated by PBGC (Pension Profit Warranty Company). This protection continues even when the variety of members turns into lower than 25 sooner or later. On account of PBGC protection, two issues occur: 1) annual premiums are paid to PBGC (a $106 flat fee or a $52 variable fee per participant in 2025), and a pair of) most profit-sharing (PS) contribution is feasible within the 401(okay) plan (as much as $70,000 in 2025). Absent PBGC protection, 401(okay) profit-sharing allocation is often restricted to six% (as you may see within the chart above).

In 2025, for instance, 6% PS could be $21,000 based mostly on $350,000 compensation, so the utmost 401(okay) and PS contribution could be $44,500. Most PS could be about 13% in a PBGC-covered plan. That is a few $25,500 distinction, and a few companions could also be sad if they can’t max out their PS. As well as, there may be some companions who don’t wish to take part within the money stability plan however who would nonetheless wish to max out their 401(okay) contribution. There are a number of choices to deal with this in a bunch that may have fewer than 25 members.

If the group is rarely going to get to 25 members and there are solely companions within the group, the Mega Backdoor Roth could be an choice. On this case, $25,500 will be contributed by way of after-tax and transformed to Roth contained in the 401(okay) plan. Alternatively, those that solely wish to contribute the 401(okay) most of $70,000 could merely contribute the distinction to the money stability plan. This can be lower than supreme, however it’s nonetheless an choice.

If the group has greater than 25 companions and/or workers, it might be doable to make the plan right into a PBGC by bringing a number of companions and/or workers into the plan to get a minimum of 25 members. This may be achieved by giving these members a significant profit, which for companions can vary from $5,000-$20,000, relying on demographics. This can be a comparatively small value to pay to make it possible for all members can max out their 401(okay). If the plan has a minimum of 25 members and all these members keep within the plan for 3 years, “significant profit” members can merely cease contributing, and the plan nonetheless retains PBGC standing with the utmost 401(okay) contribution choice for all members.

Extra info right here:

The 15 Questions You Must Reply to Construct Your Funding Portfolio

Plan Termination And Restart

In case your group has had a money stability plan for a minimum of 5 years, you in all probability questioned whether or not you may one way or the other get the cash from the money stability plan into your 401(okay) plan. There’s a technique referred to as “terminate and restart,” and it’s a authorized technique offered that a number of key situations are met. First, there have to be substantial adjustments to the plan design, and second, the plan should have been round lengthy sufficient in order that the actuaries are snug terminating and restarting it.

There are two main causes to terminate and restart your money stability plan. No. 1 is the need to maneuver your cash out of your money stability plan into your 401(okay) plan for a doubtlessly greater fee of return. No. 2 is to reduce the funding volatility danger, which turns into an actual concern as soon as the belongings within the plan develop. Even with a conservative portfolio, funding volatility can nonetheless be a priority as soon as the plan has been round for a decade or longer. Sadly, neither of those is a legitimate purpose to terminate and restart the plan.

A number of the legitimate causes for terminating and restarting your plan embody altering the plan’s curiosity crediting fee, redesigning the plan resulting from a serious shift in demographics, and merging with one other apply. Some practices could have multiple alternative to terminate and restart, however this isn’t one thing that’s assured for every apply. Basically, this technique will be carried out nearer to the 10-year mark than to the five-year mark. Whereas terminate and restart is a viable and authorized technique, one factor is definite—there is no such thing as a option to put this on a schedule (comparable to terminating and restarting each 5 years).

There are a number of sensible causes for altering the design of your money stability plan. Some plans are designed with a excessive fastened fee of return (sometimes round 5%), so to lower potential funding volatility sooner or later, a decrease fastened fee (between 3%-4%) will be chosen. If the plan will not be individually designed and has contribution ranges with caps for all members, this can be a purpose to revamp the plan to permit members to maximise their contributions. Some plans will be designed with an precise fee of return if the demographics are favorable. At this level, it ought to be clear that having a decrease crediting fee doesn’t imply that you’re one way or the other getting a decrease return in your investments. Your lifetime most is on no account affected by the crediting fee, so the one purpose to go along with a decrease fee could be both to permit for a extra favorable design (particularly in case you have workers) or to have a decrease fee to reduce funding volatility sooner or later.

The Backside Line

A money stability plan is a superb tax shelter for high-income medical doctors, however as a result of most of those plans are arrange by actuaries who’ve a really slim focus or advisers who could not have one of the best understanding of how money stability plans work, plan sponsors must get a greater thought of what’s concerned and tips on how to keep away from the forms of points that may doubtlessly show pricey.

Every apply could have completely different wants and demographics, so it is very important make it possible for your plan is designed along with your apply’s greatest pursuits in thoughts. Your apply may be candidate to terminate your plan and begin a brand new one that’s redesigned to raised match the wants of the apply. It’s uncertain that anybody would object to creating adjustments to the plan if the pursuits of all companions are protected. It’s also essential to coach any present and incoming companions about their obligations underneath your plan to make it possible for all companions are conscious of the advantages and the dangers.

It’s all the time a good suggestion to pick unbiased service suppliers who can advise the plan sponsor on one of the best plan design for the apply and who can even present fiduciary recommendation to the plan sponsor on all points of their retirement plan wants. Particularly for bigger practices, it’s important to handle future danger by taking the steps outlined above. It mustn’t value further to implement and preserve a top-notch money stability plan—a lot of the greatest methods described on this article ought to be a part of the usual set of providers and recommendation your plan ought to obtain out of your service suppliers.

Have you ever used a money stability plan? What had been the professionals and the cons? Would you employ one once more if given the possibility?

; Inventory Makes Nasdaq High Gainer Listing")

{kind=link}